Rob’s comments below are in italics.Derek’s comments below are in normal font.

We’re going to talk about interest rates on bonds today. What’s going on that people need to know about here?

Well, a few years ago, we did a piece on this. What I said was that the interest rates being commanded were a result of several different factors. One of them is the basic rate for basically hiring some money for a period. Another factor is how reliable you regard the borrower as being.

The other one was what you expected the exchange rate to move over the loan period. I probably also said that the classic way of looking at it appeared to have broken down. If you go back 10 or 15 years, the interest rates on government bonds were insanely low.

There was recently a UK Treasury bond due to mature around 2035, but trading way above par. The question is, why? We’ll come back to this, but let’s first cover the theoretical principles.

How It Should Work

The essential idea is that if somebody has a bunch of cash, they could just stick it under the bed, but the prevailing wisdom is that you want to make it earn its living. You make it earn its living by investing it in something which is going to pay you for the period that it’s tied up in that investment.

If you go to the main investment areas like the stock exchange, there are broadly two types of investment. You might get equity shares, which give you part ownership of an enterprise. Or you could make a loan, or you could put it in a deposit account in a bank, which is another way of loaning the money to the bank….

You’re actually giving the money to the bank…

Yeah, it’s no longer your money once you’ve put it in the bank. That’s another major misunderstanding that they’re very keen for most people not to realise. But we won’t get into that today. Essentially, if you look at banking in the conventional traditional way, what they’re doing is acting as an intermediary between you and their customers who want to borrow some money.

It’s a lot more complicated because, as we’ve discussed elsewhere, most of the money that the banks are lending, they’ve simply made up. They haven’t borrowed from their customers, but that’s another story for another time.

So suppose you’ve got a stack of cash and you’d like to draw an income from it. The classic position most people are in when they want to do that is thinking about being able to retire at the end of a working life. Being able to have a steady income from what they’ve accumulated over the course of a working lifetime. It’s more abstract than that for most people, but that’s what it amounts to.

As I say, the two principal ways you could invest it, apart from simply putting it in the bank and having the bank pay you interest, are either making a loan (either to the government or to a corporation, or a local government entity like the county council), or you could take part ownership of an enterprise. That’s what is called shares or equity shares.

There’s a range of risks that are associated with that. If you’re investing in a corporation that runs an operation, you might consider something very reliable, like Unilever or Procter & Gamble. There’s a very predictable amount of soap powder they’ll sell every week. There’s a very predictable profit margin on it, so it’s a very solid business. It doesn’t fluctuate much. That would be a low-risk equity.

Alternatively, you could invest in a high-tech start-up company, which might yield you an enormous return. Or it might just fizzle out and go bankrupt, and you lose the lot.

Or you might invest in a new company that has the rights to prospect where they think there’s a gold deposit. Obviously, they’ve got to spend a lot of money digging holes in the ground and seeing what they get out. If it turns out that there are nuggets of gold down there, they’ll get an enormous return for the people who invested in that. If all they dig out of the hole is a lot of dirt, you won’t get anything.

So there are high and low-risk investments. Suppose even buying shares in the soap powder company is a bit too risky. You could invest in something which is really safe.

If you go back to the 19th century, what we call gilt-edged investments or gilts for short, are government bonds. In those days the most reliable government bonds were British ones. Everybody expected the British Empire to be in business for the foreseeable future.

Right up to the early 20th century, most people made this assumption that it was going to be around forever. But it didn’t take more than a decade or two for the cracks to start appearing.

All of these things implode under their own weight in the end.

This is, of course, the lesson of history.

At that point, the British government could issue an undated bond. It had no redemption date at all. You’re basically lending your money to the British government forever on the basis that if at some point in time you want your money back, there’s always going to be somebody else who’d be prepared to take it off you.

This held up until it gradually began to fall apart after the First World War through the interwar years. Then it went rapidly downhill after that. Most of those British government bonds were around 2.5 - 3% interest. Some of them were 3.5%, depending on the prevailing circumstances when they were issued.

Suppose at a later period of time, the prevailing rate of interest is higher. Then that would mean that for each £100 nominal worth of government bonds that you’ve got, the price of the bonds would have to go down. Supposing that the prevailing rate of interest is 5%, then you’d only get £50 when you come to try and sell your £100 bond of British government debt.

The £2.50 interest on the £50 you’ve invested to get a nominal £100 would yield you 5%. It’s a straightforward ratio. If, for any reason, the interest rate went down below 2.5% or 2%, you could probably trade those 100-pound blocks for more than 100 pounds, so it would go the other way.

In recent years, since the First World War, people have been unwilling to buy undated government bonds. They would want a bond which had an expiration date when they knew they’d get the money back. This still assumes that whichever government you’ve invested in will be solvent enough to continue paying interest over the period. It’s going to be solvent enough to give you your money back when the bond expires or matures, as it’s called. Any thoughts up until this point?

So how solvent are they currently??

Well that is the big question, which is why we’re revisiting this discussion today! I’ll come back to that, but first let’s go into more detail about those other factors that set the prevailing interest rate.

We’ve covered the fact that your borrower might not be completely reliable. If you’ve got a borrower who’s not all that reliable, you’d probably want to charge a higher interest rate. You’d want to put a premium on that basic 2.5% for the rental of the money to allow for...

If I was lending money to my mates, there are certain mates that this would probably apply to!

Yeah, do you lend money to your mates?

No!

Well, that’s the point of course. If it’s all-or-nothing, then this is hypothetical. As with all statistics, you need a large base to spread your risk. If you’re talking about a single person making a single investment, it’s all or nothing. You’ve either got a reliable borrower and you get your interest paid and you get your money back at the end of the period, or you don’t, and then you lose it. But of course, if you’re thinking about something like an insurance company where you’ve got a lot of funds under your management, you’re spreading them across a lot of different people.

The idea of a risk premium makes sense. You might be lending money to the British government, the French government, the German government, and the American government. You figure that they’re not all going to go bust simultaneously, but some are looking dodgier than others. You charge them a higher rate of interest, and the others not quite as high.

Over the entire portfolio, if one or two of them go bust, then the extra income that you’ve had from the higher rate of interest would cover your losses. That’s the theory of it. If you’re moving into lending money to corporations, because corporations raise money not only from their shareholders but also from their bondholders...

They’re people who are basically lending them money. Rather than taking the risk of fluctuating interest rates, they’re assuming the corporation is solvent enough to pay a regular, reliable rate of interest, which would be lower than the interest they would expect on shares with more risk.

But this is likely to be regarded as riskier than government bonds. The other factor you need to take into account is your view on the likely inflation in the currency this bond is denominated in. If you bought Zimbabwean bonds, you might figure their currency is unlikely to hold its value. You want to really stack up the interest to take account of that.

In theory, those are the factors that set the prevailing interest in the market. A few years ago, I would have backed these factors to play out quite confidently.

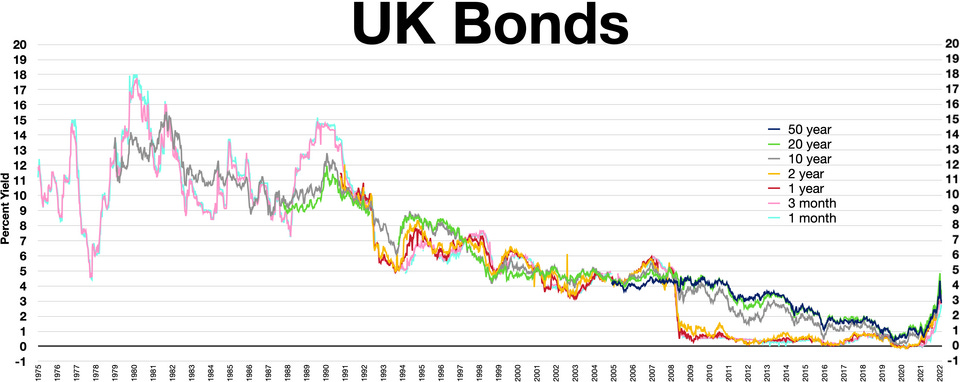

For example, when I was working in the early 70’s as an investment analyst for a stockbroking firm, we had very high inflation.It had also been only a few years since the humiliating devaluation of the pound. British government undated bonds were selling at about £16 for each 100-pound block of bonds. That was the price at which you would get the prevailing market rate, which was about 16% interest. It had to be 16% because you were taking account of the fact that your money wasn’t going to go very far when you got it back, maybe 10 years later.

The people who were buying those British undated bonds at £16 per 100, they maybe were smarter than the people who were selling them as a dead loss. Because 40 years later, the government finally decided to cash in all those undated bonds. (Foolishly, as it has turned out.) The prevailing market interest rate was then even lower than 2.5%.

Anybody who bought those bonds at £16 for the £100 worth would have been getting 16% on their interest on the money they actually spent to buy them - for the last 40 years. Then they’d have got six times as much when the government cashed them in, which obviously they did at par at £100 per bond.

Now, obviously, the bonds which have already been issued and out there in the marketplace, as we’ve just illustrated in that fairly extreme example, are going to trade at a rate which is the inverse of the prevailing interest rate. When interest rates rise, existing bonds in the market decline in price.

At the price they change hands, they’ll yield the prevailing rate of interest. If the market interest rate goes down, the price of bonds will go up. This led to a situation where the British government issued bonds that, as I say, had a maturity of 2035 or 2040.

They were originally issued at 4.25%. Then, in 2005, the prevailing interest rate was around 2%. Those 4.5% treasury bonds, maturing 30 years later, were changing hands at £220 per £100 nominal.

I thought: “This is insane. Who would spend £220 today in order to get back £100 in 30 years’ time? Who knows what the £100 is going to buy you in 30 years’ time?”

There are so many unknowns.

It was a dead cert that this was a poor investment, but that was the state of the market.

What’s Happening Today?

The reason this has come to the fore now is that the entire Western world, in particular the United States, is in a situation where all the American treasury bonds held by other countries are being allowed to expire. They’re not reinvesting in dollars. There may well be a political axe to grind in the course of that decision, but I would think that it is probably an entirely rational assessment.

First of all, they no longer need to, because over the past few years most of the rest of the world has decoupled from the need to use dollars for international trade.

Until recently, that was the only game in town, except that the chickens have come home to roost because of the way that the Americans have taken advantage of the situation to a ridiculous degree. Plus, the dollar has actually fallen quite significantly over the last year or so relative to other currencies.

It’s entirely rational that people no longer want to hold dollars, given the confident expectation that those dollars won’t buy them as much next year, the year after, or in five years’ time. That’s why these considerations of the ways that interest rates are computed are relevant today.

How’s that sound?

Yeah, to me it reiterates that we’re seeing the emergence of a multipolar world. There are definite trends moving in that direction.

Just going back to earlier in the conversation, if you’ve got money that you want to lend out and earn interest on, I was thinking of Richard Koch and his Star Principle where he talks about investing. He’s earned a lot of money by investing in small but very fast-growing companies, which is obviously quite different from a government bond, but it’s the other end of the spectrum.

Yeah, it’s the other end of the spectrum.

So, coming back to the bonds due to mature in 2035 or 2040, we reckon they were trading well over the odds. Why is that?

They were trading at that level because they had been issued at 4.5% in 2005. But after the markets had been flooded with currency by the so-called ‘quantitive easing’ in response to the crash of 2008, the prevailing market interest rate had been driven down to less than 2%. So the prices of existing bonds with higher rates moved up to keep their yield in line with that.

There’s a psychological dimension to this, as there was a lot of talk about a bond ‘bull market’. A bull market is a rising market, or one in which people have a lot of confidence, whereas a bear market is a falling market. It means people who were holding those bonds could feel good because they’d be able to sell them at a higher price.

But if they’re holding these as a safe, reliable way of getting interest, that wouldn’t actually help them. They’d make a capital gain on the bond sale, but it wouldn’t do them any good, because if they wanted to reinvest that money, it would be at the current interest rate. They’d still only be getting 2% on it.

The underlying reason interest rates were so low is that all the central banks were busy increasing the money supply. You’ve got a certain supply and demand logic in that if there’s a demand for borrowing money and there’s lots and lots of money to borrow, then you can’t charge a lot of interest for lending it.

However, like any other self-fulfilling prophecy, it has reached a point where the contradictions have become too apparent. This is what’s happening now. The central banks are stuck between cutting off the endless supply of new money, which will obviously create all kinds of solvency problems for various governments, or continuing to do so and thereby eroding confidence in the marketplace about the currency’s viability. The period of cheap borrowing for governments in the Western world is coming to an end.

You can only kick the can down the road so far…

That’s exactly it. They’ve kicked the can down the road, and this is as far as it goes. Of course, what they failed to take into account was that their hold over the rest of the world was not going to persist indefinitely.

It’s not as though the actions of China in particular, but the rest of the world in general, in diversifying out of the dollar are an attack on the dollar as such. It’s simply a preservation of their own self-interest in having put together arrangements that enable them to become more and more independent of the dollar.

The prevailing conversations around this are quite interesting. There’s an acknowledgement that the era is coming to an end. Usually, there’s a proviso added that it will take time to play out and that the dollar is still a major important currency, which it is.

But as I’ve said before, this could spiral down far more rapidly than most commentators expect. The reason is that positive reinforcing feedback mechanisms are involved. Now that the conversation has started about your dollars not buying as much in the near future, more and more people will sell, which will drive the price of dollar-denominated assets down.

Of course, the faster it goes down, the more people are going to panic and pile in. So it’s definitely going to be a very interesting few months in the very near future. We’ll see how this goes.

Watch this space is the usual way we end these episodes, and this seems to apply here. If anyone is listening to this and you have a question about something that Derek said, leave a comment below and we’ll cover it in a future episode.

Thanks for reading Sovereign Finance! Subscribe for free to receive new posts.