Welcome to The Poverty Trap, a newsletter and podcast for people who are fed up with the inequality baked into America’s system and want to individually and collectively make change.

Thinking about subscribing? Here’s what one “founding member” subscriber recently had to say about The Poverty Trap:

“You do great work, Joan. I don’t always get to read your newsletter, but when I do, I leave more informed and more compassionate…” Amy B.

__________________________________

The least pleasant event anyone wants to experience, aside from death, is losing their home. Not to sound overly dramatic, but from personal experience, the foreclosure process oftentimes can make you wish you were dead. I fought foreclosure for years, then sold my home for exactly what I owed on the mortgage during the worst of the Covid crisis. With hindsight, it might have been better for me if I had just ridden out the foreclosure moratorium in place at the time, and then let the home be sold at auction.

I survived with the help of good friends, my pets and a tough law firm, which was able to correct, on my behalf, the illegalities of the “puppy mill” foreclosure process after the fact, win compensation and a bit of extra money from the foreclosing bank as punishment for violating the law.

But losing one’s home is indeed a traumatic experience. In fact, foreclosure rates high one the scale of traumatic life experiences and can leave lasting physical and emotional scars. At that is exactly what is happening today in our country.

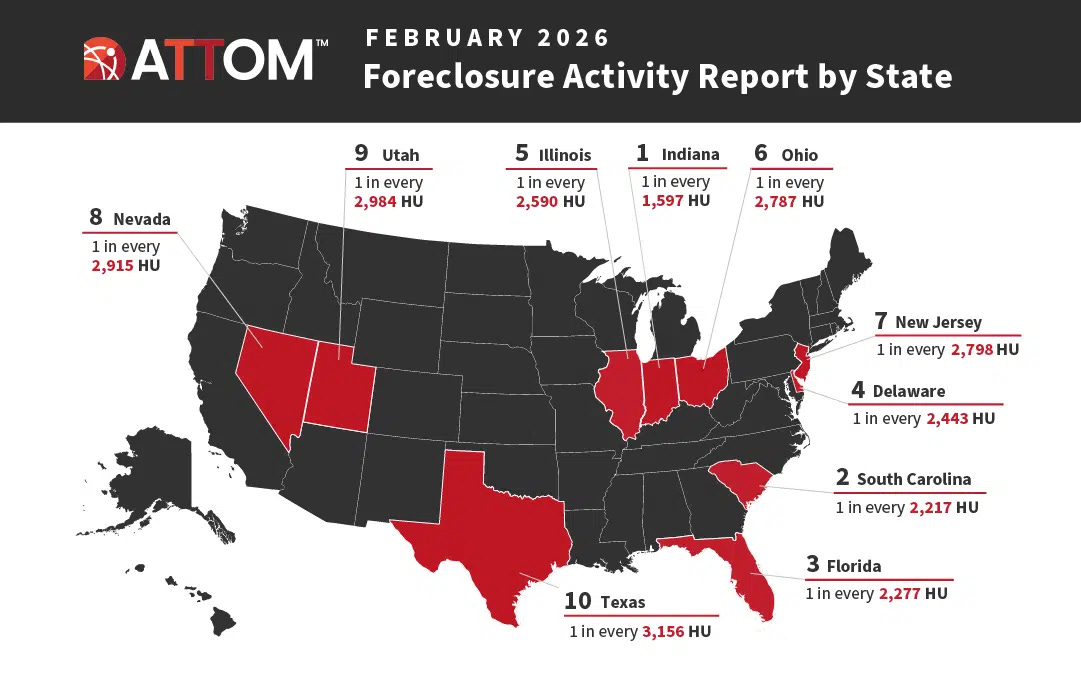

As of February 2026, foreclosure rates have increased 20%, year over year. In 2025 and into the first quarter of 2026, over 400,000 U.S. homeowners went through the nightmare of foreclosure. The five states with the highest foreclosure rates are Indiana, South Carolina, Florida, Delaware and Illinois.

There are many valid, substantive reasons for the increase in foreclosures in the last 15 months: we are trapped in a declining economy with slowed hiring, rising costs for everything, including mortgage interest rates, home insurance, property taxes, HOA fees, utilities and home repairs that make keeping a home precarious at best. Making the situation worse is the elimination of the Affordable Care Act subsidies, which allowed low and middle income earners to purchase health care at semi-affordable prices. Now, yearly costs for health care premiums are estimated to total between $23,000—$40,000 for a family of four. The choice in 2026 for many Americans looks like it’s between keeping your home or buying health insurance.

Here’s what a 2026 article from Nolo has to say about the increase in foreclosures — it primarily blames rising home-related costs, soaring prices overall and job losses for the steady increase in home foreclosures, with a gloomy future predicted:

Foreclosure activity in the U.S. is expected to trend higher in 2026.

…in 2025, there was a marked, sustained increase in both foreclosure starts and completions. According to a September 2025 report from ATTOM, foreclosure filings in the U.S. have surged nearly 20%. This upward trend could be an early indication of more trouble to come in 2026.

Yet, there seems to be a lack of expert analysis for this increase in foreclosures. Otherwise reliable property data sites, like ATTOM, are simply calling this recent increase in foreclosures a “market correction” or “normalization” of foreclosure filings. The ATTOM article noted above lays out its reasoning about rising mortgage foreclosures:

The increase reflects a continued normalization of foreclosure activity following the historically low levels seen during and immediately after the pandemic period. While filings have risen, foreclosure activity remains well below levels recorded during the housing crisis, with strong homeowner equity, tighter lending standards, and ongoing housing demand continuing to limit widespread homeowner distress…Despite these increases, overall foreclosure activity remains far below the levels seen during the housing crisis, suggesting the current rise reflects a normalization process rather than widespread homeowner distress.

What this piece fails to mention is “during and immediately after the pandemic period”, there was a national foreclosure moratorium of federally-backed mortgages in place, so of course there were historically low levels of home foreclosures during the pandemic. The same occurred during the housing crisis of the Great Recession, when there was not only a very short foreclosure moratorium, there also was an extensive federal program in place (HAMP) to help those who fell behind in their mortgage payments stay in their homes. Once HAMP fully kicked in a year or two after it was initiated, foreclosure rates dropped considerably.

Is it a valid comparison to say that today’s soaring foreclosure rates aren’t really so bad because the rates are still much lower than during a time of near economic collapse? Is it accepted thinking that banks naturally will “correct” a temporary downturn in home foreclosures which occurred during two national crises by ramping up foreclosures years later?

While the data on mortgage foreclosures are no doubt correct, the analyses fail to mention the cost to the individual and to our country, of hundreds of thousands of people losing their homes—the cost of the trauma, shame and continuing economic hardship of hardworking Americans whose paychecks can’t meet the rising price of everything.

————————————————

Please share your thoughts on the steady increase in foreclosures in the U.S., and how we should handle it. Should there be another foreclosure moratorium, given the massive increase in the cost of everything, the elimination of the health care subsidies, the war? Is it good thinking to compare this increase in home foreclosures to, say, the pandemic when there was a moratorium on foreclosures? We will all benefit from your ideas, so please leave a comment below!

The Poverty Trap is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.