Welcome to The Poverty Trap, a newsletter and podcast for people who are fed up with the inequality baked into America’s system and want to individually and collectively make change.

You might not immediately think of Mariner Finance, which does business in 27 states, as a predatory lender. After all, the company touts its community service, waves its banners at Major League Baseball games, and apparently has pleasant customer service. But it targets people who are in trouble financially, including those who have low credit scores and/or have declared bankruptcy, (Personal bankruptcy, by the way, leads directly to plummeting credit scores for 7-10 years).

This service is not all bad: it extends credit to people who could not otherwise get access to cash from more traditional lenders. The company spins it as an opportunity: “…[Mariner Finance is] an important provider of credit options to those who may have limited access to other sources of consumer credit," [Josh Johnson, founder and CEO of Mariner Finance] said.”

The problems are the origination fee, late payment fees and top tier interest rates (18% - 36% APR) that come with the typical loan from Mariner Finance. A 2025 report from Nerdwallet summarizes its practices and concludes:

Mariner Finance offers small to mid-sized personal loans online and in person. These personal loans may be an option for consumers with bad credit (629 or lower score) and those with a history of bankruptcy, but high rates and fees make this lender a less-than-ideal option for most borrowers.

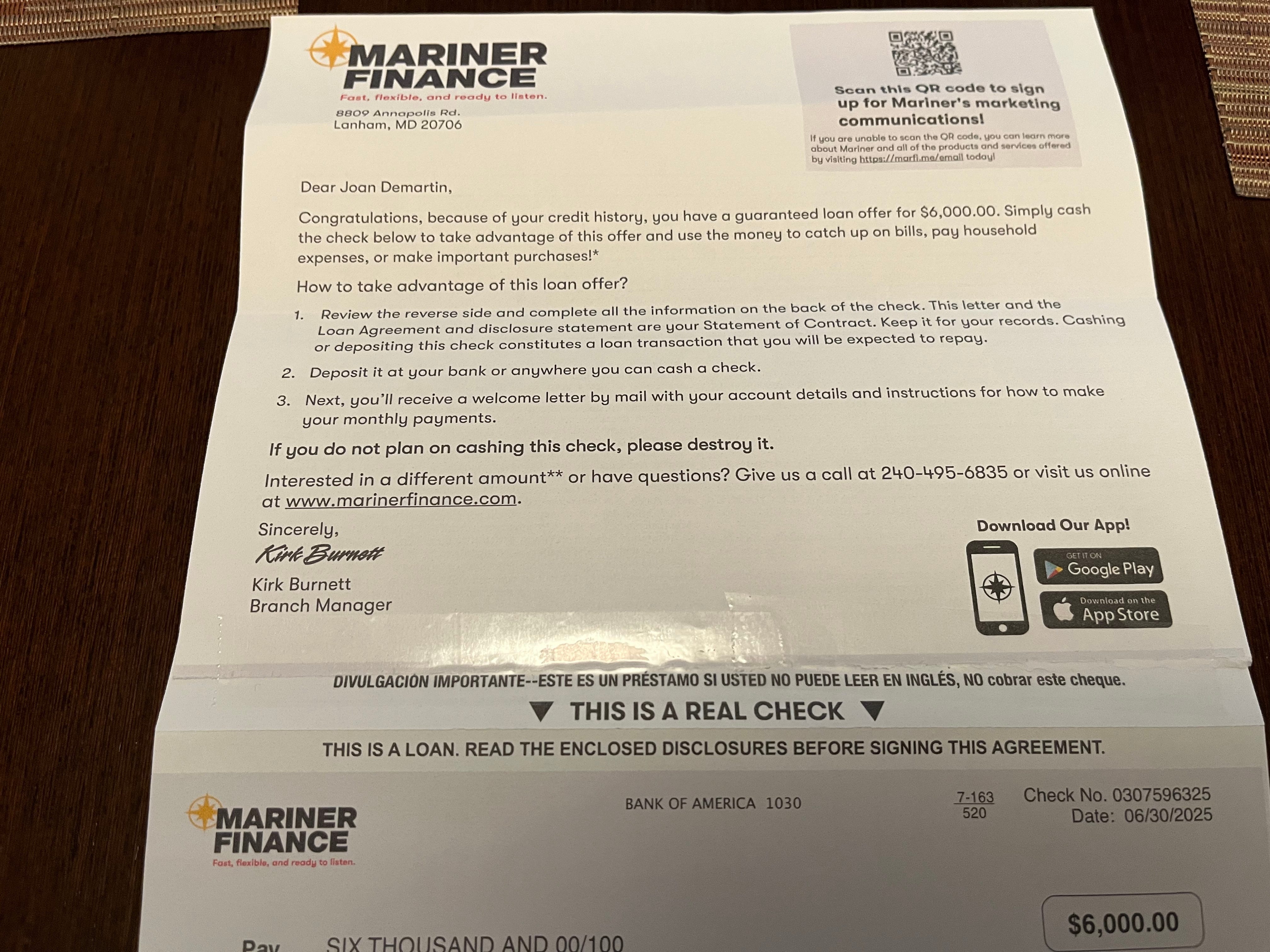

Mariner also engages in some practices that may not be consumer-friendly, like mailing checks to prospective borrowers to provide unsolicited loans. Even if you have a low credit score, it’s worth your time to compare other lenders before applying with Mariner.

There is also a problem with Mariner Finance’s deceptive loan practices. In 2022, Attorneys General from four states and D.C. sued Mariner Finance, alleging the Company saddled consumers with costly add-on insurance policies that they had never asked for or simply didn’t know were a part of their loans. This case is still ongoing, but six additional states, joined the lawsuit in 2024, and additional charges were added, including its use of “illegal, aggressive sales tactics to extend credit to new borrowers”, like the “live check” pictured above, that I recently received in the mail. According to the complaint in the updated case:

Mariner mails hundreds of thousands of unsolicited “live checks” to consumers. Once consumers cash these checks, Mariner aggressively pushes them to visit a branch to refinance and take out additional debt, which typically comes with hidden add-on products, even if it’s not in the best interest of the consumer.

North Carolina was one of the states which joined this lawsuit last year, and here’s what its Attorney General at the time, Josh Stein, said about adding its state to the suit:

But wait, there’s more. The photo below is the back of the Mariner Finance “live check’ I received. As far as I know, the language I highlighted is legal, but what borrower will read, let alone understand the importance of how their monthly payments are applied, and what it will mean to the final cost and length of their loan? In other words, the lender isn’t going to tell you in what order your loan charges will be paid off—it’s up to them.

We apply all payments you make first to late and other charges, then to Finance Charges and then to the Principal Amount, or in any other order we want. [Empasis Added].

And when there are heaps of fees, finance charges and the cost of insurance policies added to your account without your knowledge, it makes a huge difference to you that your monthly payments are applied to the original amount you borrowed dead last, after all other fees and added on charges. This means very little of your monthly payments are allocated to paying down the principal amount of the loan.

Enough about Mariner Finance, there are plenty of other predatory lenders waiting to pounce on the poor and working class. These sharks have been targeting the most susceptible, weakened consumers for decades, but the larger the financially desperate population grows, so does the lenders’ customer base. And when tens of millions of Americans are kicked off their health insurance and food stamps by “The One Big Beautiful Bill” in a year or so, predatory lenders will rake in even more profits on the backs of the our most vulnerable populations.

ProPublica published an in-depth investigative piece in late June describing predatory lenders in Tennessee titled:“You’re Already Approved: How One Tennessee Company Sets a Debt Trap”. Yes. A debt trap and a poverty trap. That company is Advance Financial, which used a loophole in a Tennessee law passed in 2014 called “The Flex Law“, that allowed a different type of loan—one that allowed pay day lenders to reborrow or rollover a customer’s original loan and borrow additional money, incurring more debt, more fees and other charges nearly impossible to pay off. In Tennessee’s original payday lending law passed in 1997, reborrowing or rolling over a pay day loan was forbidden.

Worse yet, the Flex Law’s sponsor, then Majority whip in the Tennessee house and now speaker of the House, Cameron Sexton, was also a banking executive and on the board of a local bank at the time the Flex Law was passed, and still holds both positions today. In fact, Sexton and other Tennessee lawmakers were approached by the Chairman of Advance Financial to create a new type of high-interest loan that would avoid federal oversight, he told the Nashville Business Journal. (In 2013, the Consumer Financial Protection Bureau had issued a report about the dangers of payday loans and many in the lending industry assumed federal regulations were imminent.)

Representative Sexton also received over $105,000 in contributions to his campaign and political action committee from Advance Financial and its affiliated PACs since the law was passed, making them one of his largest campaign contributors.

After enticing customers to keep borrowing, the company had no problem suing its borrowers and garnishing their wages for payback of loans it knew they could never afford —and mostly the Company won. The personal stories of the borrowers interviewed are heartbreaking—one woman wanting to buy Christmas presents for her children and grandchildren, another living on a meager disability check. According to these interviews:

All but one of the 14 borrowers who spoke to the newsrooms for this story reported having reborrowed at least once as part of their Advance loan. As with Thomas [one of the borrowers] Advance made them eligible to borrow more shortly after paying, even though they were often making the minimum payments and almost immediately borrowing the money back to cover the cost of the payment they just made. Advance went on to sue 12 of these borrowers once they stopped being able to afford the loan.

_________________________________________________

I’d love to hear your thoughts on these issues. Should payday loans be banned? Do you think the “system is rigged” against the poor, working class and average consumer? Do you see why we might need the Consumer Financial Protection Bureau to help borrowers and credit card holders escape these debt and poverty traps? Please leave your thoughts in the Comment Section below.

The Poverty Trap is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.