CLASSIFICATION: Professional Analysis, Founding Member Tier

PREPARED: 2026-05-04 | COVERAGE: April 1 to May 4, 2026 | WORD COUNT: ~10,800

REPORT TYPE: Monthly Strategic Assessment

Phase 1: Regional Stability Rankings

Region | Stability | Trend vs. March | Key Driver

--------------+-----------+-----------------+-----------------------------

Middle East | 1/10 | ▼ -1 | Iran war frozen but not

| | | ended; Hormuz blockade

| | | entrenched; UAE under direct

| | | Iranian threat

Russia/Ukr. | 3/10 | no change | Pokrovsk static after

| | | February capture; Patriot

| | | interceptor rationing; May 9

| | | Victory Day truce proposal

Europe | 3/10 | ▼ -1 | Energy shock sustained;

| | | Trump cuts 5,000 troops from

| | | Germany; transatlantic rift

| | | accelerating

North America | 4/10 | ▼ -1 | 61% of Americans call Iran

| | | war a mistake; War Powers

| | | Resolution dodged; Cuba

| | | threat

Asia-Pacific | 5/10 | no change | China managing Hormuz

| | | exposure via stockpiles;

| | | Japan/Korea worst hit;

| | | Pakistan opens land

| | | corridors with Iran

Latin America | 4/10 | ▼ -1 | Trump threatens Cuba

| | | aircraft carrier;

| | | post-Maduro Venezuela

| | | unstable; sanctions

| | | escalation

Africa | 4/10 | ▼ -1 | Russia exits Kidal (Mali)

| | | under FLA/JNIM pressure;

| | | Sahel security partnerships

| | | fracturing

Oceania/Pac. | 7/10 | no change | AUKUS holding; no direct

| | | conflict exposure; Australia

| | | oil import rerouting costs

Phase 2: Executive Summary

Bottom Line

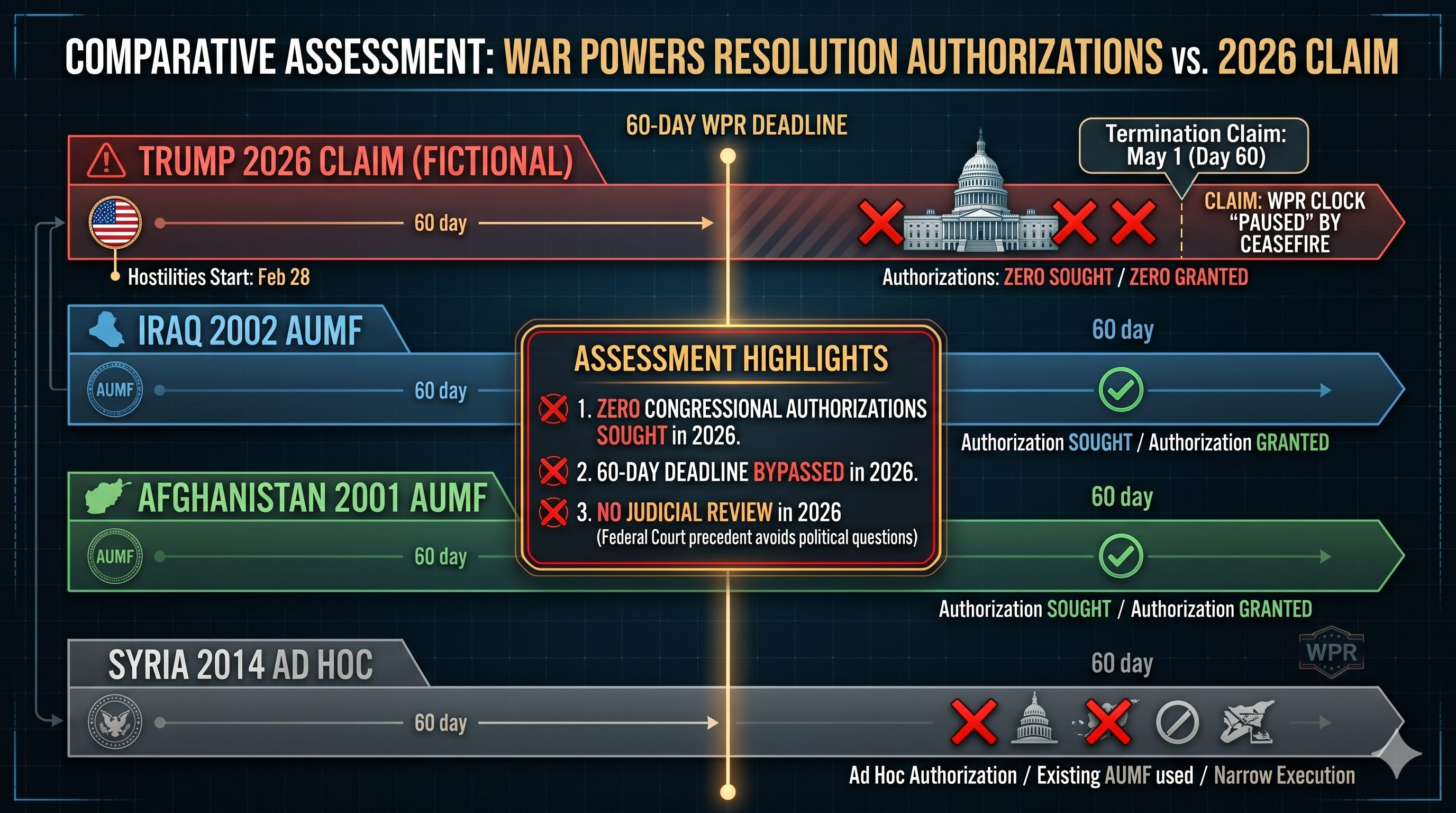

The global risk posture remains at ELEVATED (Level 4 of 5) for a second consecutive month. The defining event of April was the legal codification of the Iran war's frozen state: on May 1, President Trump notified Congress that "hostilities have terminated," dodging the 60-day War Powers Resolution deadline while simultaneously rejecting Iran's latest peace proposal and reviewing options to "blast the hell out of Iran."[1] What began February 28 as a decapitation strike that killed Supreme Leader Ali Khamenei has become something for which there is no historical analog: a war that is officially over, operationally ongoing, and structurally unresolvable.

The pattern across every region hardened in April. Trump committed publicly to an "extended blockade" of Iran's ports as US strategy, telling reporters Iran must "cry uncle" and reposting an AI-generated image renaming the Strait of Hormuz the "Strait of Trump."[2] Pakistan opened six land border crossings with Iran for cargo bypassing the maritime blockade. The UAE exited OPEC+ and was directly threatened by the IRGC. CNN's investigation found 16 US bases in the Middle East "virtually unusable" from Iranian strikes during the active phase. Brent crude traded between $100 and $126 per barrel through the month, settling near $114 by May 4.[3] Hezbollah crossed into Israel proper for the first time since the November 2024 ceasefire collapsed, deploying jam-resistant fiber-optic FPV drones imported from the Ukrainian front.[4]

The strategic transformation is now visible. The post-1991 American security architecture in the Persian Gulf, predicated on the US Navy's guarantee of Hormuz transit, has been replaced by a two-tier system: preferential passage for China, Pakistan, and selected partners; a piracy regime imposed by the United States on everyone else. Trump's own description of the policy was "We're sort of like pirates." The maritime workarounds are now structural. The diplomatic exhaustion is now permanent. The risk premium has been priced in, and it is not coming back out.

Key Strategic Signals

1. The war has been legally terminated while remaining operationally ongoing. Trump's May 1 letter to Speaker Mike Johnson and Senator Charles Grassley argued the War Powers Resolution does not apply because hostilities effectively ended with the early-April ceasefire. Defense Secretary Pete Hegseth testified that the 60-day clock "pauses or stops in a ceasefire."[5] Senator Tim Kaine (D-VA) called the interpretation legally unsupportable. Senate Majority Leader John Thune declined to schedule an authorization vote. The administration has created a precedent under which any future president can extend kinetic operations indefinitely by declaring intermittent ceasefires. Confidence: 95%. Timeframe: Permanent legal precedent.

2. The Hormuz blockade has hardened into permanent two-tier maritime governance. Iran's parliament is finalizing legislation codifying transit fees. The IRGC operates a selective passage regime granting access to Chinese, Pakistani, and Russian-flagged vessels while blocking Western shipping. Pakistan has opened six land corridors with Iran for over 3,000 containers, formally puncturing the blockade.[6] Trump's announcement of "Project Freedom" naval escorts on May 3 was contradicted by the Wall Street Journal within hours: the program consists of insurance industry coordination and mine-location tips, not actual Navy convoys. Confidence: 90%. Timeframe: Structural.

3. Iran retained operational capacity despite 64 days of attrition. Pentagon assessments leaked through CNN confirm Iran retains 60% of its ballistic missile launchers and is restoring industrial capacity to rebuild to 70% of pre-war arsenal. The Iranian Defense Ministry publicly stated only a portion of missile inventory was used during active hostilities. The IRGC successfully escorted commercial vessels through the US-declared blockade and seized at least four ships during April including the Iranian-flagged Touska, the Israeli-linked MSC Francesca, and Epaminondas. Senior US officer Joint Chiefs Vice Chairman Admiral Brad Cooper requested CENTCOM authorization to deploy the Dark Eagle hypersonic weapon for first-ever operational use against Iranian targets, citing the inability of conventional strikes to neutralize Iran's distributed launcher network. Confidence: 85%. Timeframe: Multi-year.

4. The transatlantic alliance fractured publicly and structurally. Trump ordered 5,000 US troops withdrawn from Germany over 6-12 months, framed by White House officials as direct retaliation for European non-support of the Iran operation. Pentagon internal memos obtained by Reuters explored options including Spain's NATO suspension and reversing US support of British claims to the Falkland Islands. German Finance Minister Lars Klingbeil stated on the record that Trump's war "has cut our growth in half." The Ifo Institute is forecasting German recession in 2026. Joint Chiefs Chairman General Caine accused Russia of having "assisted Iran in combat operations against American forces," a public escalation of US-Russia narrative tension despite simultaneous Putin-Trump backchannels. Confidence: 90%. Timeframe: Structural.

5. Hezbollah's fiber-optic drone capability has rendered Israeli ground operations in Lebanon unsustainable at current force structure. The Times of Israel and CNN both reported that Hezbollah is now using fiber-optic FPV drones with 10 to 15 kilometer range, immune to electronic jamming. Confirmed kills in late April and early May include a Merkava IV(M) tank, multiple NAMER and Eitan APCs, an M113 command node, and a Hermes 450 UAV.[7] The IDF formally acknowledged fiber-optic drones present a problem with no current technical solution. Hezbollah crossed into Israel proper on April 29 with an FPV strike on a vehicle in Shomera, Western Galilee, the first such attack since the November 2024 ceasefire. Israeli Channel 12 reported emergency cabinet sessions specifically on the drone threat. Confidence: 90%. Timeframe: Immediate.

6. Domestic American opposition to the war has crossed an inflection point. A Washington Post-ABC News poll on Day 64 found 61% of Americans call the Iran war a "mistake," a level the Iraq War took three years to reach and Vietnam took six.[8] Polling from Harry Enten of CNN found 55% of Republicans now blame Trump for elevated gas prices, the highest intra-party blame measurement in recorded polling. Senate Republicans blocked a Cuba war powers resolution 51-47, indicating the coalition holds for now, but the political clock on the Iran position is shorter than the structural clock on the blockade. Confidence: 85%. Timeframe: 60 to 180 days.

7. Trump's hemispheric pivot to Cuba and Venezuela introduces a parallel escalation track. Trump told reporters at the Forum Club of the Palm Beaches on May 1 that the United States will "take over" Cuba "almost immediately," suggesting an aircraft carrier will park "100 yards off the shore" on its return from Persian Gulf operations.[9] An executive order broadened US sanctions against the Cuban regime. Cuba moved its May Day parade to the Anti-Imperialist Tribune in front of the US embassy. Following the January 3 capture of Venezuelan President Nicolás Maduro in Operation Absolute Resolve and the installation of interim President Delcy Rodríguez, 90% of Venezuelans disapprove of US support for the transition government. Trump's hemispheric strategy and Iran strategy now both depend on the same Navy assets, the same political coalition, and the same finite domestic patience. Confidence: 75%. Timeframe: 30 to 90 days.

Risk Posture Assessment

The overall risk posture remains at ELEVATED, holding at the highest level since the 2022 Russian invasion of Ukraine. The deterioration vector has shifted from acute kinetic risk (active US-Iran combat, March 2026) to structural systemic risk (institutionalized maritime blockade, alliance fracture, manufactured-crisis legal precedent, May 2026). The probability of a return to active US-Iran kinetic operations within 30 days stands at 25%, rising to 40% within 90 days, with the trigger most likely an Iranian strike on UAE infrastructure or a US escort vessel. The probability of a Hormuz transit normalization within 90 days stands at 15%. The probability of regime change in Iran within 12 months stands at 10%, down from 20% in March, as Mojtaba Khamenei's leadership transition has stabilized despite minimal public exposure.

Below is the full assessment: 8 regional stability rankings, 7 strategic shifts with market implications, a probability-weighted risk matrix, alternative scenarios, and actionable portfolio positioning for equities, commodities, FX, and fixed income. This analysis synthesizes 200+ curated stories from 355+ OSINT channels, cross-referenced against Reuters, ISW, RUSI, and institutional sources. This is the caliber of work that Stratfor and Eurasia Group charge $40,000/year to deliver.

This analysis is available to Founding Members only

Phase 3: Strategic Shifts, Deep Analysis

1. The Frozen War: Legal Termination, Operational Continuation

Confidence: 95% | Impact: High | Timeframe: Permanent

Current Status

On May 1, 2026, President Trump sent a letter to House Speaker Mike Johnson and Senate President Pro Tempore Charles Grassley stating: "The hostilities that began on February 28, 2026, have terminated. There has been no exchange of fire between United States Forces and Iran since April 7, 2026." The letter, sent on the 60-day deadline imposed by the War Powers Resolution, was the administration's response to the legal requirement that the President obtain congressional authorization for sustained military operations. Defense Secretary Pete Hegseth testified before the Senate Armed Services Committee that the 60-day clock "pauses or stops in a ceasefire." Senator Tim Kaine (D-VA), who has spent his Senate career challenging executive war-making authority, told Hegseth: "I do not believe the statute would support that." Senate Majority Leader John Thune (R-SD) confirmed he would not schedule a vote authorizing force in Iran.

The factual basis of the termination claim is contested. The April 7 ceasefire collapsed within days. The US naval blockade of Iranian ports has continued without interruption since March 4. The IRGC has seized at least four commercial vessels in April including the Touska, MSC Francesca, Epaminondas, and a fourth bulk carrier. US Navy rules of engagement were updated in late April to authorize strikes on Iranian fast boats considered "immediate threats." The USS Canberra (LCS-30) was reportedly targeted by Iranian anti-ship ballistic missiles near Jask on May 3, an incident CENTCOM denied but Fars News confirmed. A US C-17A was photographed parked next to an Iranian Mahan Air aircraft at Beijing Airport on May 1, suggesting active backchannel coordination of a kind inconsistent with terminated hostilities.

Strategic Analysis

The legal innovation here is more consequential than the immediate political dispute. Trump's interpretation, that the 60-day War Powers clock "pauses" during ceasefires, would mean any President can prosecute kinetic operations indefinitely simply by inserting periodic stand-downs of any duration. The constitutional basis for the War Powers Resolution rests on the assumption that Congress can deny authorization within 60 days of hostilities commencing. If hostilities can be unilaterally declared "terminated" while operational deployments, blockades, and rules-of-engagement updates continue, the Resolution becomes a procedural ritual rather than a substantive constraint. This is not a partisan observation. The interpretation, if it stands, applies to every future occupant of the office.

The political base maintains its hold. Senate Republicans blocked a Cuba war powers resolution 51-47 on the same day Trump notified Congress on Iran. The coalition is sufficient to prevent action against the administration's interpretation. But the polling has crossed a hinge point. The Washington Post-ABC News survey finding that 61% of Americans call the Iran war a "mistake" represents a faster collapse of public support than either Iraq (3 years to reach 60%) or Vietnam (6 years). The administration is operating in a window where the political coalition holds despite majority public opposition. This window historically lasts 6 to 18 months before midterm-election dynamics force realignment.

Trajectory Assessment

At 30 days, the legal interpretation will not be challenged in court. Federal courts have consistently declined to adjudicate War Powers disputes as political questions. At 60 days, the November 2026 midterm calendar starts forcing tactical positioning. Republican incumbents in Iran-skeptical districts (Florida, Pennsylvania, Ohio) will begin distancing rhetorically while the administration absorbs the visible costs (gas prices, shipping disruptions). At 90 days, the question becomes whether Iran provides a face-saving incident that allows Trump to declare victory and accept a settlement preserving the blockade structure.

Market Implications

Equities: US defense contractors continue to benefit from accelerated munitions procurement. Lockheed Martin (LMT), Raytheon Technologies (RTX), Northrop Grumman (NOC), and L3Harris (LHX) all priced in extended sustainment cycles through 2027. Patriot interceptor manufacturer Raytheon faces particular upside given the Pentagon's admission that more than 1,200 Patriots were used in Iran operations against an annual production rate of approximately 600. Hypersonic-program contractors (Lockheed Dark Eagle, Northrop) face binary outcomes pending Trump's decision on operational deployment.

Fixed Income: US Treasury yields face structural upward pressure from extended wartime spending, an unauthorized but ongoing operational tempo, and visible Treasury issuance for new munitions production. The yield curve inversion narrative breaks if operational tempo extends.

FX: USD ambiguous. Safe-haven flows support the dollar in acute escalation scenarios but the alliance fracture (Germany troop withdrawal, NATO retaliation memo) erodes the structural reserve-currency premium over time.

Commodities: Oil maintains a $90 to $130 trading range so long as the legal frozen-war state persists. Any incident resembling a return to active hostilities triggers immediate $20+ spikes.

[CHART: War Powers Resolution timeline overlay showing congressional authorization periods (Iraq 2002 AUMF, Afghanistan 2001 AUMF, Syria 2014 ad hoc) versus Trump's 2026 termination claim. Highlight: zero authorizations sought, 60-day deadline bypassed, no judicial review.]

Recommended Positioning

Long defense sector via XAR or ITA ETFs. Long volatility (VIX) on 30 to 90 day rolling basis given binary outcome distribution. Hedge USD exposure via gold (GLD) and EUR/USD options through Q3 2026.

2. The Two-Tier Maritime System: Hormuz as Permanent Architecture

Confidence: 90% | Impact: High | Timeframe: Structural

Current Status

The Strait of Hormuz operates under a wartime governance regime that has matured into permanent architecture. Iran's IRGC Navy operates a selective passage system: preferential transit for China, Pakistan, and Russia; toll payments to the Iranian Central Bank reportedly running $2 million per vessel; and seizures of vessels from countries deemed hostile or non-compliant. The US Navy maintains nominal authority through CENTCOM declarations and a shifting carrier presence that has rotated through the USS George H.W. Bush, USS Abraham Lincoln, and most recently the USS George Washington. The USS Gerald R. Ford was pulled from CENTCOM in late April for what was described as "dire need of repair" after sustaining strikes during the active phase.

Pakistan formalized its bypass strategy by opening six land border crossings with Iran for over 3,000 containers, a move that geopolitics analysts characterized as punching "a legal loophole through Trump's blockade." The UAE exited OPEC+ on May 1, allowing it to ramp output via Fujairah and Khor Fakkan ports outside Hormuz. Saudi Arabia's East-West pipeline operates at 1.5 million barrels per day capacity. The Sumed pipeline through Egypt is running at 95% capacity. Goldman Sachs estimated Gulf crude output dropped 57% in April. JPMorgan flagged 13.7 million barrels per day removed from global supply during the month. Total global oil inventory is down 255 million barrels since February 27.

Trump's "Project Freedom" announcement on May 3 was undercut by the Wall Street Journal within hours: there are no actual US Navy escorts, only "coordinated effort by shipping and insurance companies" plus mine-location intelligence. The single tanker that transited Hormuz on the program's launch day was Iranian-flagged. Iran responded operationally on May 4 with a drone attack on a UAE-flagged tanker 78 nautical miles off Fujairah and the seizure of additional commercial shipping. TankerTrackers data shows Iran exported more oil in April than in all of March, suggesting the blockade has structural holes that neither side wants to publicly acknowledge: Iran's leverage rests on selective passage, not complete closure; the US position rests on declaring victory through sanctions enforcement, not actual blockade success.

Strategic Analysis

The post-1991 American security architecture in the Persian Gulf rested on a single proposition: the US Navy guarantees freedom of navigation through the Strait of Hormuz. Every Gulf monarchy, every European energy importer, every Asian manufacturing economy paid an implicit premium (oil priced in dollars, defense procurement aligned with the United States, willingness to sanction Iran on US timelines) in exchange for that guarantee. The guarantee is now explicitly conditional. Iran's selective passage regime demonstrates that the IRGC can deny transit to any vessel of its choosing, and the United States has no military response that does not escalate to direct kinetic confrontation it has already declared "terminated."

The architecture replacing it has three tiers: a Chinese-Russian-Pakistani-Iranian core that operates under preferential transit; a Gulf monarchy middle layer that diversifies through pipeline bypasses, OPEC restructuring, and bilateral hedging; and a Western shipping perimeter that absorbs higher insurance, longer routes, and selective bilateral exemptions. This is closer to the pre-1991 multipolar maritime regime than to the post-Cold War unipolar order. The question is not whether this configuration persists but whether it stabilizes (manageable cost increases, predictable price volatility) or destabilizes (cascading challenges to other US-guaranteed straits, the South China Sea, the Bab al-Mandeb).

Trajectory Assessment

At 30 days, Iran's parliamentary legislation codifying Hormuz transit fees passes. The legal framework outlasts any ceasefire. At 60 days, China's preferential access becomes formalized through a bilateral framework, possibly tied to Iranian crude purchases at structural discounts. At 90 days, India faces a binary choice between accepting Iranian preferential terms (annoying Washington) or continuing to absorb premium pricing (annoying domestic constituents). At 180 days, the Asian LNG market stabilizes around a new equilibrium with Qatari and US Gulf exports premium-priced and Australian and West African origins commanding scarcity premiums.

Market Implications

Equities: Maritime shipping companies (Frontline FRO, Euronav EURN, Hafnia) face elevated insurance costs and rerouting expenses that compress margins despite higher rates. Pipeline operators (Enbridge ENB, Plains All American PAA) and US Gulf LNG terminals (Cheniere LNG, Sempra SRE) capture structural premium. Asian refiners (Reliance RELI in India, Sinopec in China) face mixed outcomes depending on their access tier.

Fixed Income: Gulf sovereign debt (Saudi 30Y, UAE Dubai 10Y) is widening despite high oil prices because of infrastructure damage from Iranian strikes and forced fiscal spending on bypass infrastructure. Bahrain remains in active distress; BAPCO's force majeure has not been lifted.

FX: USD strength is contingent on perceived US capacity to enforce the blockade rather than just declare it. The CNY benefits structurally from preferential Hormuz access. Gulf pegs (AED, SAR) face managed pressure as oil revenues are routed to defensive infrastructure spending rather than reserve accumulation.

Commodities: Brent settles into a $100 to $130 structural range. WTI tracks Brent with a normalized spread of $4 to $7. Asian LNG benchmark JKM reset upward by 40% relative to Q4 2025 levels. Gold supported above $2,400 per ounce on safe-haven and central-bank diversification flows.

[CHART: Hormuz transit volumes Q1 2024 versus Q1 2026, broken down by flag of registry. Highlight: Western flag transits down 80%, Chinese flag transits up 40%, Pakistani flag transits new category.]

Recommended Positioning

Long pipeline operators (ENB, PAA) and US LNG (LNG, SRE). Short Gulf sovereign debt via CDS (BHRAIN 5Y, ADGB 10Y). Long CNH against USD as preferential-access narrative consolidates. Long Brent calendar spreads (front-month versus 6-month) to capture term-structure premium.

3. The Iran Capability Disclosure: What 64 Days of Combat Revealed

Confidence: 85% | Impact: High | Timeframe: Multi-year

Current Status

The combat phase between February 28 and the early-April ceasefire produced classified after-action assessments that have leaked progressively through April and into early May. CNN's investigation found 16 US bases in the Middle East "virtually unusable" from Iranian missile and drone strikes during the active phase. Camp Arifjan in Kuwait was described as a destroyed "microcity." Camp Buehring in Kuwait took a successful F-5E fighter strike with conventional bombs, evading Patriot interceptors. NBC and CBS confirmed Iranian fixed-wing aircraft penetrated US air defenses to bomb regional bases during the opening phase, a capability the Pentagon had previously assessed as nonexistent. Pentagon assessments shared with congressional committees confirmed Iran retains 60% of its ballistic missile launchers and is restoring industrial capacity to rebuild to 70% of pre-war arsenal. Iran's Defense Ministry publicly stated that only a portion of missile inventory was used during active hostilities.

Joint Chiefs Vice Chairman Admiral Bradley Cooper's request to deploy the Dark Eagle Long-Range Hypersonic Weapon for first-ever operational use against Iranian targets is the most consequential disclosure of the month. The US Army's Long-Range Hypersonic Weapon, Dark Eagle, achieved declared operational capability in late 2024. It has never been used in combat. The request reflects Pentagon judgment that conventional cruise and ballistic strikes cannot reliably neutralize Iran's distributed launcher network. Admiral Cooper's reported framing was that the US military "can no longer hit Iran's launchers." Trump received a 45-minute briefing on options described publicly as "blast the hell out of Iran" and "finish them forever," but no operational order has been issued. Amazon Web Services confirmed that Iranian strikes on its UAE cloud region during the active phase caused damage requiring months to fully restore, an unprecedented disruption to a major-cloud-region by state actor strikes.

US Tomahawk inventory is reportedly more than one-third depleted relative to pre-war levels. Half of THAAD and Patriot interceptor stockpiles were expended. The Department of Energy is requesting $99 million for accelerated production of anti-bunker nuclear munitions, a category that includes the B61-12 variants and the GBU-57A/B Massive Ordnance Penetrator. The MOP is the conventional weapon that was reportedly used against Fordow during the opening phase with results that the Pentagon has not publicly assessed.

Strategic Analysis

The decapitation thesis underlying the February 28 operation, that killing Khamenei plus overwhelming air power would force Iranian capitulation, has been definitively falsified. Mojtaba Khamenei's succession appears stable despite his remaining largely out of public view, with a confirmed major message issued for May 1 Persian Gulf Day. The IRGC's "Mosaic Defense" doctrine, which distributes command authority across regional commanders to survive precisely this kind of decapitation attempt, performed as designed. The combination of distributed leadership, dispersed launchers, civilian-defense mobilization (Basij), and selective-passage maritime leverage produced a state that is more difficult to coerce than the United States anticipated.

The capability disclosures matter beyond Iran. China is conducting its own assessment of the campaign. The combat performance demonstrates that Iran's anti-access/area denial systems, comprised of mostly Russian and indigenous technology, can impose 16-base degradation on a force projection campaign by the world's most capable military. The implications for any future Taiwan contingency are substantial: Chinese A2/AD systems are an order of magnitude more capable than Iran's, and the geographic conditions are more favorable to defense. The Pentagon's Tomahawk and Patriot expenditure rates over 64 days are not sustainable in a Taiwan contingency that would likely run measured in years. Russian Defense Minister Andrei Belousov's meeting with Iranian Deputy Defense Minister Nasser Talaei-Nik in Kyrgyzstan late in the month suggests technology and lessons-learned exchange flowing in both directions.

Trajectory Assessment

At 30 days, the Pentagon completes a classified after-action review and presents Trump with a Dark Eagle operational deployment recommendation. The decision is binary: deploy and risk validating Iranian survivability claims, or hold and accept that the conventional strike option cannot resume against current Iranian defenses. At 90 days, Iran's missile arsenal restoration crosses the 50% threshold in the Pentagon's own assessment. At 180 days, the next-generation Iranian missiles incorporating combat lessons (improved evasion, better terminal guidance, longer ranges) begin operational deployment.

Market Implications

Equities: Hypersonics primes Lockheed Martin and Northrop Grumman face binary outcomes. Lockheed's Conventional Prompt Strike (CPS) Navy variant, built on the same Common Hypersonic Glide Body as Dark Eagle, would likely be procured at accelerated rates if Dark Eagle is deployed. Air-defense primes RTX and General Dynamics face structural multi-year procurement upside given Patriot/THAAD depletion. Cloud infrastructure vulnerability (AMZN, MSFT, GOOGL) gets a sober reassessment from enterprise risk teams; expect modest re-rating of physical-resilience premium for hyperscaler valuations.

Fixed Income: Defense procurement is a multi-year fiscal commitment that adds sustained pressure to Treasury yields. The 10Y sustained above 4.5% becomes the new equilibrium.

FX: Defense imports from US to allies create dollar-positive flows. Counterbalancing this, Russian and Chinese defense exports gain market share in the global south, reducing dollar dominance over time.

Commodities: Steel, aluminum, copper, and rare earths face structural demand from defense-industrial base reshoring. Antimony, gallium, and germanium (Chinese export-controlled) face acute constraint.

Recommended Positioning

Long defense primes via PowerShares Aerospace & Defense (PPA) ETF. Within sector, prefer interceptor and hypersonics over platform primes. Short cloud hyperscalers' 12-month forward multiples through Q4 options.

4. The Hezbollah Ceasefire Collapse and the Drone Inversion

Confidence: 90% | Impact: High | Timeframe: Immediate

Current Status

The November 2024 Israel-Hezbollah ceasefire that ended the 2024 war collapsed structurally during April 2026. Israel's "yellow line" buffer construction in southern Lebanon, intermittent IDF airstrikes, and the demolition of civilian infrastructure (including the historic Christian monastery in Yaroun and 20 border settlements per New York Times reporting) created the operational pretext for Hezbollah's return to active engagement. By late April Hezbollah had crossed into Israel proper for the first time since the ceasefire, conducting an FPV drone strike on a vehicle in Shomera, Western Galilee. Multiple Israeli media reports confirmed an emergency cabinet session focused specifically on the fiber-optic drone threat.[4]

The technology shift is the strategic story. CNN, Times of Israel, and i24News all reported that Hezbollah is now operating fiber-optic guided FPV drones imported from the Ukrainian theater. These drones are physically tethered to operators by 10 to 15 kilometer fiber-optic cables, making them immune to Israeli electronic warfare jamming. Component cost ranges from a few hundred dollars to $4,000 per unit. Confirmed kills in late April and early May include a Merkava IV(M) main battle tank in Qantara on April 28 (the first confirmed video kill of an Israeli MBT in the conflict), multiple NAMER and Eitan APCs, an M113 command node, and a Hermes 450 UAV downed by SAM near Nabatieh. The IDF has formally acknowledged having no current technical solution to the fiber-optic drone threat.

The reciprocal escalation has been Israeli airstrike intensity. Israel struck 120 Hezbollah targets over a single weekend in late April. Suspected white phosphorus use in Baraacheet was reported by multiple Lebanese and Arab outlets. The Lebanese Ministry of Health is reporting both military and civilian casualties from sustained Israeli operations. Knesset Foreign Affairs Committee Chair Boaz Bismuth stated publicly that "the Iranian regime is about to pay a very heavy price," tying Lebanon operations explicitly to Iran. US Secretary of State Marco Rubio confirmed the United States is building "vetted units" inside the Lebanese Armed Forces to disarm Hezbollah, an unprecedented level of direct US intervention in Lebanese internal security architecture.

Strategic Analysis

The fiber-optic drone is the most consequential ground-warfare innovation since the Russia-Ukraine war introduced FPV drones in volume. The Russia-Ukraine theater proved FPV drones could destroy main battle tanks, APCs, and artillery at price points that invert the ratio of attack to defense. Russian and Ukrainian forces both initially relied on radio-controlled FPVs that could be jammed by electronic warfare systems mounted on vehicles. The fiber-optic variant, developed by both sides during 2024 to 2025, removes the jamming countermeasure entirely. The cost of attack falls below $4,000. The cost of replacing a destroyed Merkava IV approaches $7 million. The cost of training a tank crew runs into hundreds of thousands. The exchange ratio favors the attacker by orders of magnitude.

For Hezbollah specifically, fiber-optic drones solve the operational-depth problem. The IDF's air superiority and electronic warfare capabilities had previously made Hezbollah forward operations costly and short. Operators can now control engagements from 10 to 15 kilometers behind the front, in protected positions, with effectively unjammable links. This converts every ceasefire violation by Israeli forces in southern Lebanon into a high-risk engagement for Israeli armor and infantry, while Hezbollah can sustain operations from positions that pre-fiber doctrine could not have justified. The implication for any future Israeli ground operation in Lebanon is that the manpower-replacement cycle Chief of Staff Lt. Gen. Eyal Zamir warned of in late March, in which the IDF "collapses in on itself" from manpower shortages, accelerates substantially.

Trajectory Assessment

At 30 days, Hezbollah's fiber-optic drone tempo continues at current rates with the IDF unable to deploy a technical countermeasure. The political pressure on Netanyahu's coalition (already cited by Israeli press as having Bennett favored as a possible replacement) intensifies. At 60 days, either Israel accepts a renegotiated Lebanon ceasefire that codifies its retreat from positions south of the Litani River or it commits to a manpower-intensive ground operation that Zamir has warned is unsustainable. At 90 days, the absence of an effective Israeli response begins reshaping deterrence calculations across the region (Hamas, Houthis, Iraqi Popular Mobilization Forces) about Israeli capability constraints.

Market Implications

Equities: Israeli equities (TA-35 index) face downside as coalition stability deteriorates and operational tempo strains the economy. Defense contractors with counter-drone product lines (AeroVironment AVAV, Anduril private, RTX) gain procurement upside. Israeli technology firms with significant US listings (Wix WIX, Mobileye MBLY, CyberArk CYBR) face country-risk discount.

Fixed Income: Israeli sovereign debt (10Y ILS) widens approximately 50 to 80 basis points relative to mid-April levels. Lebanese sovereign remains in default territory; sustained operations elevate humanitarian and reconstruction-funding exposure for international donors.

FX: Israeli shekel under structural pressure. Bank of Israel intervention has been observed but is unlikely to prevent further depreciation if operational tempo escalates.

Commodities: Modest upward pressure on natural gas (Israeli-Egyptian Leviathan and Tamar fields proximate to conflict zone). The Karish field, struck during the 2024 round, remains a vulnerability.

Recommended Positioning

Short Israeli equities via inverse exposure (selective). Long counter-drone defense names. Hedge Israeli debt exposure via CDS. Long shekel volatility through quarterly options.

5. The Transatlantic Fracture: Germany, NATO, and Strategic Decoupling

Confidence: 90% | Impact: High | Timeframe: Structural

Current Status

President Trump ordered the withdrawal of 5,000 US troops from Germany on a 6-12 month timeline at the end of April. White House officials briefed reporters that the decision was direct retaliation for European non-support of the Iran operation. Trump suggested in subsequent remarks the eventual cut would be "a lot further" than 5,000. Secretary of Defense Hegseth told reporters: "We don't rely on Europe, but they need the Strait of Hormuz much more than we do. Maybe it's time to stop talking so much." Pentagon internal memos obtained by Reuters explored options to punish NATO members who did not support Operation Epic Fury, including Spain's NATO suspension and reversal of US support for British claims to the Falkland Islands. The administration has not formally adopted these proposals but their existence represents a step previous administrations would not have considered.

German Finance Minister Lars Klingbeil stated on the record that Trump's war "has cut our growth in half." The Ifo Institute's Clemens Fuest is forecasting German recession in 2026, with Q1 GDP declining 0.6% quarter-on-quarter and Q2 expected to print negative. German industrial production has contracted 4.2% year-on-year. Energy-intensive sectors (chemicals, steel, paper, automotive) face permanent capacity reduction as gas prices remain structurally elevated post-Hormuz crisis. The European Council formally adopted the €90 billion ($105 billion) interest-free loan to Ukraine on April 23, with Slovakia and Hungary dropping their objections after extensive negotiation. The 20th sanctions package targeting Russia's shadow fleet and energy revenues passed simultaneously.

Joint Chiefs Chairman General Caine accused Russia of having "assisted Iran in combat operations against American forces," a public escalation despite Trump's simultaneous 90-minute call with Putin during which the Russian President offered to mediate the Iran nuclear impasse. Putin publicly offered a May 9 Victory Day ceasefire in Ukraine. The US "supports" the proposal per administration statements, though no operational pause has been agreed. Russian Defense Minister Belousov stated: "Moscow and Tehran will support each other under any circumstances." A USAF C-17A photographed parked next to an Iranian Mahan Air aircraft at Beijing Airport on May 1 suggests active US-China-Iran backchannel coordination notwithstanding public hostilities.

Strategic Analysis

The transatlantic alliance has survived multiple stress tests since 1949: De Gaulle's NATO withdrawal in 1966, the Suez crisis of 1956, the Iraq War split of 2003, and Trump's first-term tariff disputes. The April 2026 sequence is structurally different. Previous frictions involved disagreements within a shared strategic framework. The current sequence involves the United States deliberately punishing European NATO members for failing to support a war the United States itself has now declared "terminated," combined with proposed administrative actions (Spain suspension, Falklands revisitation) that would treat allies as adversaries. The European response has been to accelerate strategic autonomy: the €90 billion Ukraine loan represents the largest unitary European defense commitment in history; the 20th sanctions package shows continued capacity for unanimous action despite Hungarian and Slovak resistance.

The most consequential structural shift is the reorientation of European defense industrial planning toward independence from US suppliers. France has accelerated procurement of indigenous missile and drone capabilities. German Chancellor Merz has shifted rhetoric from "burden sharing" to "European pillar," language that previous administrations would have considered alliance-threatening. The UK has hedged by maintaining bilateral deals with the United States while signaling alignment with French strategic autonomy proposals. Italy and Spain are positioning to absorb European-funded defense procurement that previously would have flowed to US contractors.

Trajectory Assessment

At 30 days, the Trump administration's planned Spain action (NATO suspension or formal sanction) faces internal resistance from State Department and Pentagon professional staff. The action is unlikely to be formally taken but the threat permanently degrades US standing. At 60 days, German recession is confirmed in official Q2 statistics. The political consequences in Berlin force Chancellor Merz toward harder positioning. At 90 days, the European Defense Industrial Strategy is announced with specific procurement targets that exclude US primes from approximately 40% of new contracts through 2030.

Market Implications

Equities: European defense primes (Rheinmetall RHM, Thales HO, Leonardo LDO, BAE Systems BA./L) capture multi-year structural upside. US primes face share loss in European procurement decisions. Industrial conglomerates with European exposure (Siemens, Schneider Electric) face mixed outcomes depending on energy intensity.

Fixed Income: German bunds remain under cyclical pressure as recession is priced in, but structurally bid as European safe-haven. Eurozone periphery (Italian BTPs, Spanish bonos) face widening on political risk. Treasury Inflation-Protected Securities (TIPS) attract bid as European energy-import inflation persists.

FX: EUR/USD ranges between 1.05 and 1.12 with structural weakness from energy import burden and recession risk balanced against European unity premium and US fiscal deterioration. Sterling under pressure as UK navigates between French autonomy and US alliance.

Commodities: European natural gas (TTF benchmark) sustains €60+ per MWh through summer 2026. European industrial commodity demand (steel, aluminum, copper) compresses by 8-12% relative to 2024 levels.

[CHART: NATO defense industrial procurement flows 2014 to 2026, broken down by US share versus European share. Highlight: structural decline in US share from 65% in 2014 to projected 45% by 2028.]

Recommended Positioning

Long European defense via Stoxx Europe 600 Aerospace & Defense (EXX1.DE). Short European industrials with high energy intensity. Long EUR/USD volatility via quarterly options. Long German bunds at 30Y duration through Q4 2026.

6. The Hemispheric Pivot: Cuba, Venezuela, and Parallel Escalation

Confidence: 75% | Impact: Medium-High | Timeframe: 30 to 90 days

Current Status

President Trump told reporters at the Forum Club of the Palm Beaches in West Palm Beach on May 1 that the United States will "take over" Cuba "almost immediately." The President described an aircraft carrier, suggested as the USS Abraham Lincoln, parking "100 yards off the shore" on its return from Persian Gulf operations, at which point Cuba "will say, thank you very much, we surrender." Trump signed an executive order broadening US sanctions against the Cuban regime; the Trump administration has now imposed over 240 sanctions and intercepted at least seven tankers, cutting Cuban oil imports by 80% to 90%. Cuba responded by relocating its May Day parade to the Anti-Imperialist Tribune in front of the US embassy in Havana under the slogan "The Homeland Is Defended," presided over by Raúl Castro and Miguel Díaz-Canel. The Senate blocked a Cuba war powers restraining resolution 51-47 on May 1.[9]

The Cuba escalation occurs against the backdrop of the January 3 capture of Venezuelan President Nicolás Maduro and his wife Cilia Flores in Operation Absolute Resolve. Interim President Delcy Rodríguez has overseen what 90% of Venezuelans tell pollsters is a failure to restore democratic transition. 94% of Venezuelans say Rodríguez is moving too slowly. Cuba's First Secretary Díaz-Canel labeled the January operation "state terrorism" and declared two days of national mourning for the 32 Cuban personnel killed protecting Maduro. The US capture was the first overt US military operation aimed at South American regime change.

Strategic Analysis

Trump's hemispheric strategy is a coherent geographic concept ("Western Hemisphere first") executed with the same operational improvisation as the Iran campaign. The aircraft carrier-as-deterrent visit concept Trump described publicly is operationally infeasible: a Nimitz-class carrier cannot safely approach within 100 yards of a defended coastline. The actual operational concept being studied is more limited: targeted strikes on regime infrastructure, intelligence cooperation with Cuban opposition, sanctions enforcement against tankers. The political concept is broader: convert Cuban regime collapse into a domestic political win that compensates for Iran's perceived strategic ambiguity.

The risk vector is the simultaneity. The same Navy assets, the same authorization structures, the same political coalition, and the same finite domestic patience cannot indefinitely sustain three concurrent strategic theaters: Iran extended blockade, Venezuela post-capture stabilization, and Cuba escalating coercion. Each theater individually is manageable; collectively they exceed the doctrinal capacity of US force projection. The Gerald R. Ford was pulled from CENTCOM in late April for repair. The USS Abraham Lincoln carrier strike group is reportedly the prospective Cuba deployment vehicle. Routing through the Caribbean from Persian Gulf operations adds 14 to 21 days transit time during which neither theater has the asset.

Trajectory Assessment

At 30 days, sanctions enforcement intensifies against Cuban tanker imports. Energy shortages on the island become acute. Cuban regime stability is tested but holds, similar to the 2021 protests. At 60 days, either an aircraft carrier deployment occurs as a signaling event (likely in late June or early July) or the threat is downgraded as operational realities constrain the option. At 90 days, the 2026 midterm primary calendar starts forcing Republican incumbents to position on a potentially open-ended Cuba operation. At 180 days, either a regime collapse scenario plays out (consistent with Trump's stated objectives) or the position consolidates into a maximum-pressure status quo.

Market Implications

Equities: Caribbean cruise lines (Carnival CCL, Royal Caribbean RCL, Norwegian NCLH) face short-term volatility on any escalation. Florida-based real estate and financial services firms face mixed outcomes. Energy traders specializing in Latin American oil flows face acute volatility as Cuba supply routes are disrupted.

Fixed Income: Latin American sovereign debt faces broad widening on regional contagion. Argentine and Peruvian dollar bonds face the cleanest exposure. Mexican peso volatility increases as the United States demonstrates willingness to use military force in the region. Hard-currency Cuban debt remains in default territory.

FX: Mexican peso (USDMXN) volatility increases. Brazilian real (USDBRL) directly exposed to Petrobras-Cuba trading relationship. Colombian peso exposed to migration pressure if Cuban or Venezuelan instability accelerates.

Commodities: Cuban nickel exports (the country is the world's seventh largest producer) face supply disruption risk. Sugar markets exposed but less acute. Caribbean shipping rates face premium during any escalation phase.

Recommended Positioning

Short Mexican peso via near-term forwards. Long Latin American sovereign debt CDS as basket trade. Hedge Caribbean tourism equity exposure via puts. Long nickel through Q3 2026.

7. The Information Transparency Inversion: OSINT Versus State Communication

Confidence: 80% | Impact: Medium | Timeframe: Structural

Current Status

The Iran war has accelerated a structural transformation in geopolitical information flows that began with the Russia-Ukraine conflict. Traditional state communications channels (presidential statements, press briefings, official military assessments) have been comprehensively contradicted by OSINT, satellite imagery, social media verification, and embedded reporting from non-traditional outlets at scales not previously observed. Trump's claim that "we crushed Iran with conventional weapons" is contradicted by Pentagon assessments leaked through CNN that Iran retains 60% of launchers. Trump's "Project Freedom" announcement was contradicted by the Wall Street Journal within hours. Trump's "Strait of Trump" rebrand and "Iran has no navy, no air force, no anti-aircraft" claims are contradicted by IRGC operational tempo, F-5E strikes on Camp Buehring, and air defense activations across multiple Iranian provinces.

The disclosure of Camp Arifjan's "virtually unusable" status, Amazon's UAE cloud region damage, Patriot interceptor depletion rates, and the Dark Eagle deployment request all came through journalist sources rather than Pentagon press briefings. The IRGC has shifted to releasing high-quality video documentation of ship seizures (MSC Francesca, Epaminondas) within hours of operational completion. Russian propaganda and Iranian state media have professionalized to the point where individual posts attract 30,000+ engagement on translated platforms. The fiber-optic drone inversion is being documented in real time by both Hezbollah and Israeli sources, accelerating doctrinal assessment cycles by orders of magnitude.

Strategic Analysis

The structural shift is from a hierarchical information architecture (state channels primary, citizen sources secondary) to a distributed verification architecture (multiple independent sources cross-referenced, state channels treated as one source among many). The implications for democratic decision-making are mixed. On one hand, the public has access to higher-fidelity information about active military operations than at any point in modern history; the 61% "mistake" polling on Iran has formed in 64 days because citizens can verify state claims against independent sources in near-real-time. On the other hand, the same architecture creates vulnerability to coordinated disinformation campaigns, manufactured controversy, and weaponized narrative cascades.

The market implications run through a different mechanism than political consequences. Hedge funds, family offices, and institutional traders have re-architected their geopolitical research operations during 2024 to 2026 to incorporate OSINT verification. Bloomberg Terminal data, traditional newswire feeds, and government-source reporting are now treated as one input among many. The price-discovery function is now distributed across satellite imagery firms (Maxar, Planet), shipping data providers (TankerTrackers, Windward), social media verification services (Bellingcat, Janes), and OSINT research aggregators. The premium for first-mover information advantage has compressed substantially. The premium for synthesis and judgment has expanded correspondingly.

Trajectory Assessment

At 30 days, more disclosures from the active phase emerge through journalist channels as classification reviews release more material. At 90 days, the Pentagon's formal after-action review is delivered to congressional committees, with classified and unclassified versions. At 180 days, academic and think tank assessments of the campaign begin appearing in publication, providing the first systematic doctrinal analysis. At 12 months, the full strategic implications are absorbed by US defense planning, Chinese assessment cells, and global military doctrine.

Market Implications

Equities: OSINT and satellite imagery providers face structural demand growth. Maxar Technologies (private, owned by Advent International), Planet Labs (PL), BlackSky (BKSY) all positioned for multi-year growth. Bloomberg LP and other traditional information providers face margin pressure as their information moats erode.

Fixed Income: Sovereign credit pricing faces compression of information advantage; rapid news cycles drive shorter holding periods and increased turnover. Credit spread volatility structurally elevated.

FX: Reaction speeds to geopolitical events accelerate, compressing arbitrage windows. Algorithmic FX strategies that incorporated traditional news flows face displacement by OSINT-informed approaches.

Commodities: Oil and shipping markets price information faster, with implied volatility structurally elevated. Specialized commodity research firms gain market share against generalist coverage.

Recommended Positioning

Long satellite imagery and OSINT-adjacent equities (PL, BKSY). Short legacy financial information providers on multi-year horizon. Long volatility products (VIX futures, oil implied volatility) on rolling basis through 2026.

Phase 4: Alternative Scenarios and Tail Risks

Scenario Distribution (12-Month Horizon)

Base Case (60%): Frozen War Stabilization. Trump's "extended blockade" doctrine consolidates as official US strategy. Iran's parliamentary legislation codifying Hormuz transit fees passes by mid-2026. Two-tier maritime governance becomes the new equilibrium. Brent crude trades $90 to $130 with periodic volatility on incidents. Hezbollah-Israel low-intensity conflict continues with the IDF unable to deploy effective fiber-optic countermeasures. Mojtaba Khamenei consolidates leadership with minimal public exposure. Domestic American opposition crystallizes around 60-65% "mistake" polling but Republican coalition holds through midterms. The transatlantic alliance survives in degraded form with European strategic autonomy advancing structurally.

Upside Case (15%): Negotiated Resolution. Putin's mediation offer creates the back-channel framework for an Iran-US framework agreement. Iran accepts a face-saving structure: nominal return to JCPOA-style enrichment caps in exchange for sanctions relief, formal Hormuz transit fee recognition, and US naval drawdown from Persian Gulf operations. Brent settles at $75 to $90. The Hezbollah front stabilizes around a renegotiated Lebanon ceasefire. Israeli coalition fractures and Bennett succeeds Netanyahu. Trump declares strategic victory and pivots to domestic agenda for the midterm cycle.

Downside Case (20%): Escalation to Kinetic Resumption. A trigger event (Iranian strike on UAE infrastructure, US carrier vessel hit, Kuwait sovereign incident) breaks the frozen war. Trump deploys Dark Eagle hypersonics against Iranian targets. Iran responds with regional escalation including potential Saudi Aramco strikes. Brent breaches $150. Asia-Pacific energy import economies (Japan, Korea, India) face acute fuel rationing. The transatlantic alliance fractures further as European leaders publicly oppose escalation. The 2026 midterms become a referendum on Iran policy with substantial Republican losses.

Tail Risk (5%): Multi-Theater Escalation. Cuba military action triggers Venezuelan resistance, Russian deployment to Cuba (echoing 1962), and broader hemispheric conflict. Simultaneous Iran kinetic resumption combined with Hezbollah-Israel ground war and Houthi Bab al-Mandeb closure overwhelms US force structure. Patriot interceptor depletion forces rationing decisions between Israel, Saudi Arabia, and Taiwan. China observes US overextension and accelerates Taiwan timeline. Brent breaches $200. Global recession deepens.

Hidden Risks Not Currently Priced

Iranian succession instability. The Mojtaba Khamenei transition has held thus far but is not yet tested by a meaningful operational reverse or political challenge. A successful Israeli decapitation strike against Mojtaba (which Israeli Defense Minister Israel Katz publicly stated Israel is "waiting for an American green light" to attempt) creates immediate succession uncertainty within an IRGC-dominated structure. The probability is currently low (15%) but the impact would be high.

Saudi-Iranian rapprochement collapse. The 2023 China-brokered Saudi-Iran normalization has held through the war despite Iranian strikes on Gulf infrastructure. A direct Iranian strike on Aramco facilities or Saudi sovereign infrastructure breaks the framework. Saudi entry into the US-Israeli coalition would dramatically increase Iranian operational pressure but also increase regional escalation risk.

Pakistani internal instability. Pakistan's mediation role and land-corridor opening have held despite UAE pressure (the UAE demanded $3.5 billion in IMF loan repayment from Pakistan during mediation). Army Chief Asim Munir's role is increasingly central. Internal Pakistani instability or a successful assassination would disrupt the mediation framework that is currently containing escalation.

US carrier vessel loss. No US Navy capital ship has been struck during the conflict despite multiple reported attempts. A successful Iranian or Houthi anti-ship cruise missile or ballistic missile strike on a US carrier or destroyer would represent the first such event since World War II and force domestic political realignment.

Chinese Taiwan opportunism. China has observed 64 days of US capability expenditure, alliance strain, and political distraction. The window for opportunistic Taiwan action is narrowing as Pentagon assessments and Patriot replenishment proceed, but the assessment that Beijing is building a "decision space" for Taiwan operations is increasingly common in US intelligence community analysis.

Phase 5: Regional Assessments

Middle East: Stability 1/10

The defining month of the modern Middle East. The Iran war, declared "terminated" by President Trump on May 1 while operational tempo continued, has restructured regional security architecture in ways unlikely to be reversed. The frozen-war state consolidates institutional facts: Iran's selective Hormuz transit regime, the IRGC's seizure capability against commercial shipping, Hezbollah's fiber-optic drone inversion of the Israel-Lebanon force balance, and the Pakistan-Iran land corridor bypass of the maritime blockade.

Iran's strategic posture has stabilized despite 64 days of attrition. Mojtaba Khamenei's succession is consolidating, with major public messages issued for May 1 Persian Gulf Day affirming Iranian sovereignty over the Gulf and rejecting US demands. The IRGC retains 60% of pre-war launcher capacity per Pentagon assessment. Iranian missile production is restoring industrial capacity. Foreign Minister Abbas Araghchi's diplomatic tour (Pakistan, Oman, Russia) demonstrates that Iran retains strategic partnerships including direct mediation channels through Putin. Iran's "final proposal" delivered through Pakistan in late April was rejected by Trump but its 14-point framework (3-phase, 30-day timeline, uranium enrichment capped at 3.5%) provides a baseline that any future settlement must engage.

Saudi Arabia and the UAE are positioning between hedging and exposure. The UAE exit from OPEC+ on May 1 allows expanded production via Fujairah and Khor Fakkan ports outside Hormuz, but the IRGC threat to UAE infrastructure (publicly delivered in late April) and the May 4 drone strike on a UAE-flagged tanker 78 nautical miles off Fujairah place Abu Dhabi in direct exposure. Saudi Arabia is increasing East-West pipeline utilization and pursuing a quieter diplomatic posture. Both Gulf monarchies face pressure from Washington and Beijing to choose alignment in the new two-tier maritime regime.

Israel's coalition stability is the most acute regional question. Hezbollah's ceasefire collapse, the fiber-optic drone capability, and the IDF manpower crisis combine to create operational pressure unprecedented since the 1973 war. Bennett is now publicly favored by some polls to succeed Netanyahu. Defense Minister Israel Katz's statement that Israel is "waiting for an American green light to annihilate the Khamenei dynasty" reflects coalition desperation rather than capability. The Lebanon front consumes IDF resources without producing strategic gains, while the southern Lebanon civilian destruction (20 settlements leveled per New York Times) generates international condemnation without reducing Hezbollah operational capability.

The most consequential trajectory variable is the US response to the operational continuation of the war it has legally terminated. Trump's framework forces a binary choice within 30 to 90 days: either accept Iran's structural gains (Hormuz tolls, distributed missile capability, regional alliance leverage) by allowing the frozen war to stabilize, or escalate via Dark Eagle deployment or comparable kinetic options. Either outcome reshapes the region for a generation.

Europe: Stability 3/10

The transatlantic fracture moved from rhetorical to structural in April. Trump's order to withdraw 5,000 US troops from Germany, framed as direct retaliation for European non-support of the Iran operation, represents the most consequential alliance reordering since Charles de Gaulle's 1966 withdrawal of France from NATO's integrated military command. The Pentagon's internal exploration of options including Spain's NATO suspension and reconsideration of US support for British Falklands sovereignty crossed an institutional threshold previous administrations would not have approached.

Germany faces simultaneous economic and security stress. The Ifo Institute's recession forecast for 2026, with Q1 GDP at -0.6% quarter-on-quarter and German industrial production contracting 4.2% year-on-year, reflects the structural cost of Hormuz-driven energy prices on Europe's largest economy. Finance Minister Klingbeil's on-record statement that Trump's war "has cut our growth in half" is unprecedented in postwar German-American relations. Chancellor Merz has shifted rhetoric toward "European pillar" language that would have been considered alliance-threatening in any previous administration.

The European Union demonstrated continued capacity for collective action. The €90 billion Ukraine loan adopted by the European Council on April 23 represents the largest unitary European defense commitment in history. Hungary and Slovakia, having extracted concessions, dropped their objections to both the loan and the 20th sanctions package targeting Russian shadow fleet and energy revenues. The European response to Trump's troop withdrawal is to accelerate strategic autonomy: France leads procurement of indigenous missile and drone capabilities; Germany rebuilds its defense industrial base; the UK hedges by maintaining bilateral US ties while signaling alignment with French autonomy.

Energy security remains the binding constraint. European TTF gas prices sustain at €60+ per MWh through summer 2026. Storage levels heading into winter 2026-2027 face structural shortfall absent a Hormuz normalization. The shelving of the planned permanent Russian oil ban remains in effect. Italian Deputy Prime Minister Salvini called publicly for a return to Russian gas purchases. Russia retains energy leverage over Europe that the 2022 sanctions architecture was specifically designed to eliminate.

Trajectory: at 30 days, the Spain action (formally adopted or quietly shelved) clarifies the administration's institutional capacity for radical alliance restructuring. At 90 days, the European Defense Industrial Strategy is announced with specific procurement targets that exclude US primes from approximately 40% of new contracts through 2030. At 12 months, the post-NATO European security architecture begins emerging in observable form.

Russia/Ukraine: Stability 3/10

The Russia-Ukraine conflict entered its fifth year with tactical stasis and strategic shift. The Pokrovsk-Myrnohrad sector, captured by Russian forces in early 2026, has not seen meaningful Russian advance since December 2025. Ukrainian defenders held through 16 Russian assault attempts in a single April day, with the front line stabilizing along Hryshyne, Bilytske, Nove Shakhove, and Rodynske. Russian losses continued at 900 to 1,040 personnel per day per Ukrainian MoD reports. The Pokrovsk-Myrnohrad ruins serve as Russian logistics corridor, generating attrition without territorial gain.

The strategic shift comes from Patriot interceptor rationing. Pentagon allocation decisions are visibly favoring Israel and the Persian Gulf over Ukraine. Ukrainian leaks indicate Patriot deliveries have slowed substantially since the Iran war began. The implication for Russian strategic targeting is to accelerate cruise missile and drone strikes on Ukrainian energy infrastructure ahead of winter 2026-2027. Russian forces struck Odesa overnight April 23 to 24, killing two and damaging a maternity hospital and schools. The Dnipro apartment building strike on April 22-23 killed three. Russian campaign intensity is increasing as Ukrainian air defense erosion proceeds.

Putin's diplomacy is the structural innovation. The 90-minute Putin-Trump call in late April produced two operational outputs: Putin offered a May 9 Victory Day ceasefire (which the US "supports" but neither side has implemented), and Putin offered to mediate the Iran nuclear impasse. Russian Defense Minister Belousov publicly stated "Moscow and Tehran will support each other under any circumstances." The convergence of Russian-Iranian strategic positions reflects shared interest in disrupting US extended deterrence in both Eastern Europe and the Middle East simultaneously.

The European Council's €90 billion Ukraine loan, adopted April 23, replaces declining US support with European fiscal commitment. The transfer represents both a relief mechanism for Ukraine and a stress test of European unity. Slovakia's Robert Fico and Hungary's Viktor Orbán dropped their objections after extensive negotiation; future objections from new political coalitions cannot be ruled out. The 20th sanctions package targeting Russian shadow fleet and energy revenues passed in parallel.

Trajectory: at 30 days, Russian campaigning intensity continues with limited tactical success. At 60 days, May 9 Victory Day passes without operational ceasefire. At 90 days, Ukrainian air defense degradation forces hard rationing decisions on which infrastructure to protect. At 12 months, either a negotiated ceasefire emerges through Russian-American backchannels or Ukrainian defensive collapse becomes a real risk in 2027.

North America: Stability 4/10

US domestic conditions are visibly degrading on both political and economic dimensions. The Washington Post-ABC News poll finding 61% of Americans call the Iran war a "mistake" represents faster collapse of public support than Iraq (3 years to reach 60%) or Vietnam (6 years). Harry Enten's CNN polling finds 55% of Republicans now blame Trump for elevated gas prices. The political coalition holds in the Senate (51-47 blocking the Cuba war powers resolution) but is increasingly visible as a coalition of incumbents protecting an unpopular position rather than executing a coherent agenda.

The War Powers Resolution dodge sets a constitutional precedent. The administration's interpretation that the 60-day clock "pauses or stops in a ceasefire" effectively eliminates the Resolution as a meaningful constraint on executive war-making for any future administration. Senate Majority Leader Thune's refusal to schedule an authorization vote completes the procedural inversion: Congress neither authorized nor disauthorized the war; the administration declared termination unilaterally; the institutional architecture for democratic war-making has been replaced by executive declaration.

Economic conditions reflect the structural cost of the Iran war on US household balance sheets. Gas prices remain elevated. Spirit Airlines declared bankruptcy on May 3, citing fuel costs as the proximate cause. US Treasury yields are structurally elevated as the market prices in extended wartime spending and visible Treasury issuance for new munitions production. The Dollar Index (DXY) has held its safe-haven bid through volatility but the structural reserve-currency premium is eroding as alliances fracture.

The hemispheric pivot to Cuba (sanctions, threatened aircraft carrier deployment) and Venezuela (post-Maduro stabilization failure under Rodríguez) introduces additional fronts that the same political coalition and same Navy assets must support. Trump's May 1 statement that the United States will "take over" Cuba "almost immediately" was met with Senate authorization restraint blocking but no operational commitments. The simultaneous management of Iran, Cuba, Venezuela, and Ukraine commitments stresses force structure beyond doctrinal capacity.

Trajectory: at 30 days, the November 2026 midterm primary calendar starts forcing Republican incumbents in Iran-skeptical districts toward distancing rhetoric. At 60 days, gas prices and consumer sentiment data force tactical moderation in administration messaging. At 90 days, midterm campaign positioning becomes the dominant constraint on continued escalation. At 12 months, either a successful resolution narrative emerges or Republican losses reshape both Congress and 2028 succession dynamics.

Asia-Pacific: Stability 5/10

China managing exposure with strategic discipline. Asian energy importers absorbing the Hormuz disruption with varied success. The region's stability rating reflects the absence of direct conflict combined with significant economic stress flowing through energy channels.

China's strategic posture combines preferential maritime access (Beijing has secured continued Hormuz transit for COSCO bookings to Gulf states), substantial strategic petroleum reserves (over 120 days of net imports per Windward analysis), and disciplined diplomatic communication. The USAF C-17A photographed parked next to an Iranian Mahan Air aircraft at Beijing Airport on May 1 reflects active US-China-Iran coordination beneath public hostilities. Trump's April 23 remark that "We caught a ship yesterday with some things on it that weren't very nice. A gift from China, perhaps. I am surprised" (regarding the Touska seizure) was followed by lower-tone commentary acknowledging "we do the same thing with other countries." The active hostilities are managed; the structural competition continues.

Japan, South Korea, and India face the highest direct exposure. Japanese LNG spot prices in the JKM benchmark are running 40% above Q4 2025 levels. South Korean refiners face force majeure declarations on Iranian crude that they had been quietly continuing to source. India faces a binary choice between accepting Iranian preferential terms (annoying Washington) or continuing to absorb premium pricing (annoying domestic constituents). Pakistan opened six land border crossings with Iran for over 3,000 containers, formally puncturing the maritime blockade and demonstrating that Asian supply alternatives are emerging.

Taiwan operates in the shadow of US capability constraints visible in the Iran campaign. Pentagon Tomahawk and Patriot expenditure rates are not sustainable in a Taiwan contingency that would likely run measured in years. China's assessment of US force projection limits is being conducted in real time. The risk is not immediate Chinese action but expanded "decision space" that previous Pentagon planning assumed would remain narrow. Australian Prime Minister Albanese's government has accelerated AUKUS submarine procurement and bilateral defense dialogue with Japan and South Korea.

ASEAN economies face both energy disruption and shipping rerouting costs. Singapore's Changi-based airline Scoot ranked first globally for lowest emissions in 2025 but faces fuel cost pressure. Thai Foreign Minister Sihasak Phuangketkeow publicly stated that China told Bangkok it is "struggling to free 70 of their own ships." Indonesia and the Philippines face direct exposure through Japanese and Korean supply chain disruption.

Trajectory: at 30 days, Asian LNG market reaches new equilibrium. At 60 days, China-Iran preferential bilateral framework is formalized. At 90 days, India makes its choice between Iranian access and US alignment. At 180 days, Taiwan strategic environment is reshaped by US capability disclosure and Asian regional realignment.

Latin America: Stability 4/10

Latin America faces a parallel escalation track that maps onto but does not yet directly intersect with the Iran theater. Trump's threats against Cuba, the post-Maduro Venezuelan transition, and broader hemispheric posture combine to create a regional risk profile sharper than any since the Cold War.

The post-January 3 Venezuela transition is observably failing on its stated democratic objectives. Interim President Delcy Rodríguez has overseen what 90% of Venezuelans tell pollsters is a stalled or non-existent return to democracy. 94% of Venezuelans say Rodríguez is moving too slowly. The Trump administration's approach has shifted from the original "regime capture for democratic transition" framing to a maximum-pressure incumbency that resembles regime co-optation more than reform. The downstream implications for migration, Colombian-Venezuelan border dynamics, and Brazilian regional positioning are substantial.

Cuba escalation accelerated dramatically in late April and early May. Trump's May 1 statement at the Forum Club of the Palm Beaches that the United States will "take over" Cuba "almost immediately" combined with the executive order broadening sanctions and the Senate's 51-47 blocking of restraint. Cuba's response of relocating the May Day parade to the Anti-Imperialist Tribune signals continuing regime confidence in popular mobilization. The 240+ sanctions and tanker interceptions cutting Cuban oil imports by 80-90% create acute economic pressure but have not produced regime instability.

Mexico faces structural exposure through the United States demonstrating willingness to use military force in the hemisphere. President Claudia Sheinbaum has maintained diplomatic distance while accelerating bilateral defense and migration dialogues. Mexican peso volatility has increased visibly. The 2026 USMCA renegotiation begins in this environment, with Mexican leverage compressed.

Brazil under President Lula has positioned for Latin American multilateralism that excludes both Washington and Caracas alignment. Brazilian-Cuban energy trade through Petrobras has been complicated by US sanctions enforcement. The BRICS framework continues to expand but the operational coordination remains limited.

Argentina under President Milei has aligned closely with the United States on regional questions, including support for the Venezuela transition and skepticism of Cuban regime survival. The economic relationship with the IMF continues stabilizing. The political relationship with Brazil and Mexico has cooled substantially.

Trajectory: at 30 days, the Cuba aircraft carrier deployment either materializes or is downgraded. At 60 days, Venezuelan migration patterns from continued instability begin pressuring Colombia and Peru. At 90 days, the regional realignment around Trump-aligned (Argentina, El Salvador, Ecuador) versus multilateralist (Brazil, Mexico, Colombia) blocs hardens.

Africa: Stability 4/10

The Russian Africa Corps deployment in the Sahel suffered its most consequential setback of the war on April 26, when joint operations by the Tuareg-led Azawad Liberation Front (FLA) and the al-Qaeda-affiliated Jama'at Nusrat al Islam wal Muslimin (JNIM) forced Russian fighters out of Kidal in Mali. Russian personnel reportedly negotiated their exit through Algerian mediation. The withdrawal demonstrates that the Wagner-to-Africa Corps transition has not produced operational continuity. Discontent among Malian officers, some of whom have privately expressed preference for "more professional and disciplined partners," reflects growing strain in the Russian security partnership model.

The 2,500 Russian Africa Corps personnel deployed in Mali, 100 in Niger, and 100 to 300 in Burkina Faso represent a substantial commitment that is producing diminishing operational returns. The Sahel security partnership architecture that replaced French Operation Barkhane is fracturing under both insurgent pressure and Russian internal organizational difficulties (the Wagner Group's transition to formal Defense Ministry authority degraded operational autonomy). The June 2024 to early 2025 period during which Wagner appeared to deliver tactical results against insurgents has been replaced by a defensive posture that the Africa Corps doctrinal model favors.

The implications for African sovereign positioning are substantial. ECOWAS members are reassessing the cost of Russian security partnership relative to alternative frameworks. Senegalese President Bassirou Diomaye Faye has reopened dialogue with European partners on counterterrorism. Nigerian President Bola Tinubu has hedged through enhanced US-Nigeria military cooperation while maintaining BRICS positioning. South African President Cyril Ramaphosa continues balancing BRICS leadership with selective Western engagement.

The Horn of Africa faces continued volatility. Yemen's Ansar Allah (Houthi) entry into the Iran war in late March opened a second maritime chokepoint risk at the Bab al-Mandeb Strait. Houthi missile and drone capabilities continue degrading Red Sea shipping despite US Navy presence. Ethiopian-Eritrean tensions persist around Tigray. Sudan's civil war continues without meaningful diplomatic progress.

North African positioning has consolidated. Egypt under President Sisi has positioned as Sunni mediator with simultaneous channels to Israel, Iran, and Gulf states. The Egyptian government's snub of Syrian President Ahmed al-Sharaa at the Cyprus summit demonstrated regional skepticism of the Syrian transition. Algerian mediation in Mali demonstrates expanded regional diplomatic role. Moroccan-Saharan dynamics continue without direct conflict but with persistent diplomatic friction.

Trajectory: at 30 days, the Mali security situation deteriorates further, with the FLA-JNIM coalition potentially threatening additional towns. At 60 days, ECOWAS membership questions for Mali, Niger, and Burkina Faso reach decision points. At 90 days, the Russian security partnership model faces its first meaningful country-level reversal as a Sahel government potentially renegotiates terms or pursues alternative arrangements.

Oceania/Pacific and Antarctica: Stability 7/10

The region maintains the highest stability rating in the assessment, reflecting the absence of direct conflict exposure combined with structural alignment with the AUKUS framework. Australia, New Zealand, and the Pacific Island Forum members face indirect exposure primarily through energy supply chains and trade rerouting costs.

Australian Prime Minister Anthony Albanese's government has accelerated AUKUS Pillar 2 implementation, with the second tranche of advanced capability programs (hypersonics, AI, cyber, electronic warfare) entering active development phase. The Virginia-class submarine acquisition timeline is on track for first delivery in early 2030s. Australian defense spending is targeting 2.4% of GDP by 2027, exceeding the previous 2030 target. The bilateral defense dialogue with Japan has progressed to interoperability framework implementation; the trilateral structure with the United States and Japan formalized in November 2024 is now producing joint operational planning.