August 27, 2025

[This is Part 4 of a 5-part series on the hidden history of money and power, continuing from “Revolution and Greenbacks: America’s Monetary Insurgency.”]

“First they ignore you, then they laugh at you, then they fight you, then you win.”

— Often attributed to Gandhi (though he likely never said it)

“Unless they change the laws. Then you lose.”

— Every monetary reformer ever

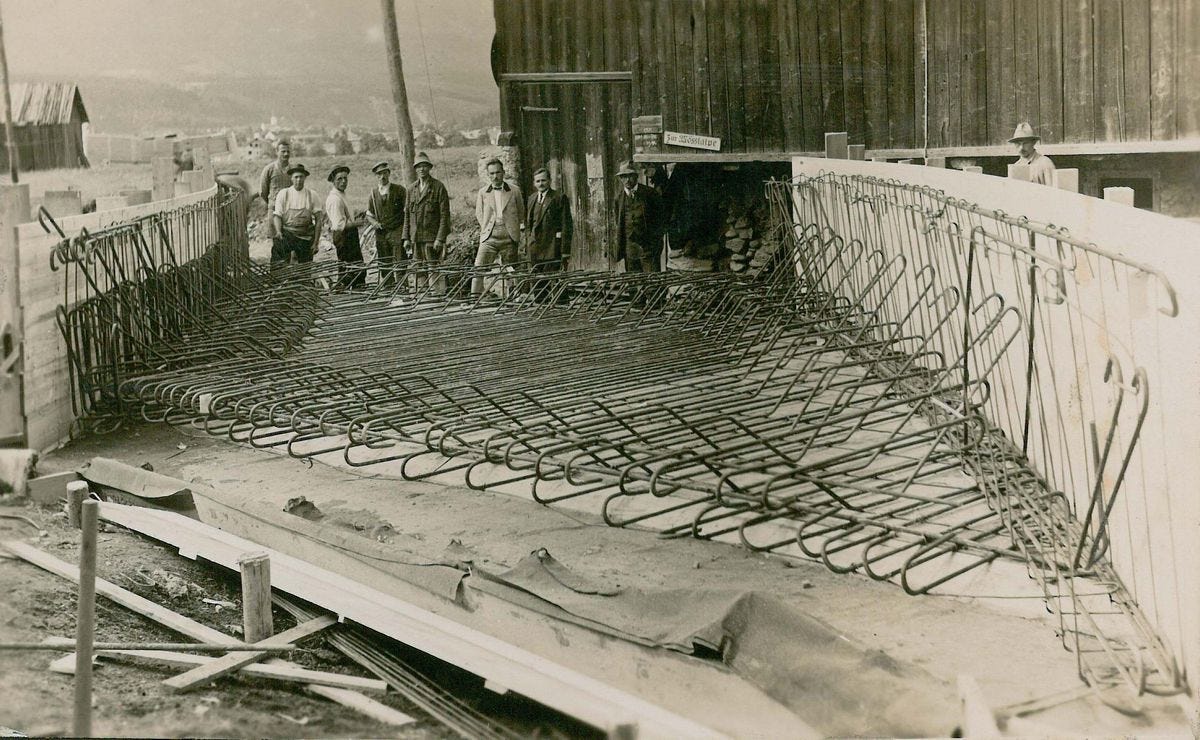

The bridge built in Wörgl, Austria, during its “miracle” year of 1932-33. Constructed with local currency while the rest of the world descended into depression. The experiment was so successful it had to be destroyed. Photo: Unterguggenberger Institute, https://unterguggenberger.org/the-free-economy-experiment-of-woergl-1932-1933/

Wörgl, Austria: A Town That Defeated the Depression, 1932

In the summer of 1932, the Austrian town of Wörgl was dying. Of its 4,216 inhabitants, 1,500 were jobless. The local factory had shuttered. Farmers couldn’t sell their produce. The town government, broke and unable to collect taxes, had laid off workers and halted all public projects. In the cemetery, suicides were being buried at night to avoid the shame.^[1]

Wörgl’s mayor, Michael Unterguggenberger, was an unlikely monetary revolutionary. A social democrat who’d worked his way up from the railroad yards, he lacked formal economic training. But he’d been reading the works of Silvio Gesell, a German-Argentine businessman who proposed a radical theory: that money itself was defective. Not this currency or that currency, but the very concept of money as traditionally understood.^[2]

Gesell’s insight was simple but profound. Money serves two incompatible functions:

* Medium of exchange (facilitating trade)

* Store of value (preserving wealth)

The problem? When money stores value perfectly, people hoard it, especially during uncertain times. This hoarding removes money from circulation, causing recession. Gesell’s solution was “Freigeld” (free money) - currency that depreciated over time, forcing circulation.^[3]

On July 31, 1932, Unterguggenberger convinced the Wörgl town council to try something unprecedented. They would issue their own currency: “Certified Compensation Bills” that lost 1% of their value each month. To maintain full value, holders had to affix a stamp costing 1% of the note’s face value. This created a powerful incentive: spend it or lose it.^[4]

What happened next has been called “the miracle of Wörgl,” though it was really just mathematics:

Month 1-3: The town paid workers with the new currency for public works. Workers, not wanting to pay the stamp tax, spent quickly at local shops. Merchants, facing the same incentive, immediately paid suppliers or taxes.

Month 4-6: Tax revenue increased by 35% as people rushed to pay with depreciating currency. The town launched new projects: paving streets, building a reservoir, constructing a ski jump.

Month 7-12: Employment fell by 25% while Austria’s unemployment rose by 20%. The velocity of money - how fast it circulated - was estimated at 14 times higher than the national schilling.

Month 13: The Austrian National Bank sued to stop the experiment. By court order, Wörgl’s currency was declared illegal.^[5]

“I can see that the Wörgl currency has convinced everybody that money doesn’t have to be gold or government notes, but can be whatever a community agrees to use. This is dangerous knowledge.”

— An Austrian Central Bank official, 1933 (quoted in regional newspaper)

The data from Wörgl’s experiment was stunning:

* 100,000 schillings of local currency created economic activity equal to 2.5 million schillings

* The currency circulated 463 times in 13.5 months (vs. 21 times for regular currency)

* Town revenue increased despite tax cuts

* Full employment achieved while surrounding towns suffered 30% unemployment^[6]

The experiment attracted international attention. Irving Fisher, America’s most famous economist, visited to study it. The French Premier Édouard Daladier dispatched observers. Over 200 Austrian towns prepared to launch similar systems.^[7]

Then it was crushed.

Local Currencies vs Austrian Supreme Court, 1933

The Austrian National Bank’s case against Wörgl was straightforward: only the central bank could issue currency. The town’s “Certified Compensation Bills” violated the bank’s monopoly. It didn’t matter that Wörgl’s currency was fully backed by official schillings deposited in a bank. It didn’t matter that it had saved the town from economic collapse. It didn’t matter that it was voluntary - no one was forced to accept it.

What mattered was the precedent. If one town could issue currency that worked better than the national money, what would stop others? If local currencies could eliminate unemployment while the central bank’s policies failed, what justified the central bank’s existence?

The court proceedings were a foregone conclusion. On September 1, 1933, Austria’s Supreme Court ruled Wörgl’s currency illegal. The town was ordered to redeem all outstanding notes immediately. Within weeks, Wörgl sank back into depression. The workers who’d built the bridge returned to breadlines. The suicide rate resumed its climb.^[8]

Unterguggenberger fought on, traveling Europe to promote monetary reform. But history was turning dark. The Nazis, who’d initially supported Gesell’s ideas, abandoned them for traditional economics after taking power. Unterguggenberger died in 1936, broken by the return of the misery he’d briefly conquered.^[9]

“The monetary monopoly is the achilles heel of the State. Challenge it, and you challenge everything.”

— E.C. Riegel, monetary theorist

Bad Money Creates Good Money, Good Money Creates Bad Actors…

Meme truths

Wörgl wasn’t unique. Throughout history, successful monetary alternatives have been systematically destroyed - not for failing, but for succeeding. The pattern is consistent:

Step 1: Crisis - Economic depression creates desperationStep 2: Innovation - Local communities create alternative currenciesStep 3: Success - The alternatives work, often spectacularlyStep 4: Suppression - Central authorities kill the experimentsStep 5: Erasure - The success is forgotten or dismissed

This pattern repeated across the globe during the Great Depression:

United States: Stamp Scrip Movement, 1933

By 1933, hundreds of American communities had launched currencies modeled on Gesell’s ideas. The most successful:

Hawarden, Iowa: The town issued $300 in stamp scrip that generated $100,000 in economic activity over 15 months. Merchants reported business increasing by 40%.^[10]

Pella, Iowa: Their stamp scrip circulated so rapidly that the city collected enough revenue to pay off civic debts early.

Russell, Kansas: The local chamber of commerce issued “Russell-ites” that put 200 unemployed back to work.

Over 300 communities had operating scrip systems by March 1933. Yale economist Irving Fisher calculated that properly designed stamp scrip could end the Depression within weeks. He prepared legislation for a national stamp scrip system.^[11]

Then Franklin Roosevelt took office. On March 4, 1933, he issued an executive order effectively banning all “emergency currencies.” The New Deal would reflate the economy through federal spending and banking reforms - not local monetary innovation. Within months, America’s scrip experiments died.^[12]

Germany: Wära Experiment, 1930

Before Wörgl, the German town of Schwanenkirchen tested Gesell’s theories in 1930. A closed coal mine was reopened, paying workers in “Wära” - currency that depreciated 1% monthly. The results:

* The mine went from 0 to 1,000 employees

* Local unemployment virtually disappeared

* Surrounding regions accepted Wära for trade

* Over 2,000 businesses eventually participated^[13]

The Reichsbank killed it in 1931, declaring private currencies illegal. The mine closed. The workers returned to bread lines. Two years later, desperate Germans would elect anyone promising jobs.

Canada: Alberta Social Credit, 1935

During the Depression, the Canadian province of Alberta elected a radical government promising monetary reform. The Social Credit party, led by William “Bible Bill” Aberhart, won 56 of 63 seats in 1935 by promising to issue “prosperity certificates” - essentially provincial currency.^[14]

The experiment barely launched before Ottawa crushed it. The federal government:

* Disallowed provincial monetary legislation

* Threatened to withhold federal transfers

* Had the Supreme Court declare provincial currency unconstitutional

* Forced Alberta back into line^[15]

France: SEL Systems, 1990’s

Even in modern times, the pattern continues. In the 1990s, France saw an explosion of “Systèmes d’Échange Local” (SEL) - local exchange systems using alternative currencies. By 1996, over 300 SEL groups operated across France, facilitating trade without euros.

The most successful, in Ariège, had 1,000 members exchanging millions in value annually. Local unemployment dropped. Small businesses thrived. Communities strengthened.^[16]

Then the tax authorities intervened. SEL transactions were declared taxable in euros - even though no euros changed hands. Unable to pay taxes on non-euro income, most SEL systems collapsed. The survivors operate in legal grey zones, careful not to grow large enough to attract attention.

Germany’s Hidden Success: Sparkassen, 1778

Not all alternatives are killed. Some survive by avoiding direct confrontation with central banking power. Germany’s Sparkassen (public savings banks) represent the world’s most successful alternative banking model - hidden in plain sight.^[17]

Founded in the late 18th century, Sparkassen operate on principles that would horrify Wall Street:

* Public ownership: Owned by municipalities, not shareholders

* Public mandate: Required to serve local communities, not maximize profit

* Boring banking: Focus on savings and small business loans, not speculation

* Local restriction: Can only operate in their home regions

* Profit recycling: Surpluses fund local projects, not executive bonuses^[18]

The results speak for themselves:

* 431 Sparkassen with 15,000 branches serve every German community

* They hold 40% of all German deposits

* They provide 43% of all loans to businesses and households

* They finance 60% of Germany’s Mittelstand (small/medium enterprises)

* They weathered 2008 without bailouts while Deutsche Bank nearly collapsed^[19]

During the 2008 crisis, as global banks froze lending, Sparkassen increased loans to local businesses. While American communities watched local banks get swallowed by Wall Street giants, German towns kept their financial institutions. While British banks paid billions in bonuses after taxpayer bailouts, Sparkassen funded local theaters and youth programs.

“Sparkassen are like bumblebees. According to aerodynamics, they shouldn’t be able to fly. According to economics, they shouldn’t be profitable. Yet they fly and profit anyway.”

— German banking analyst

The secret to Sparkassen survival? They never challenged the monetary system itself. They work within it while serving different masters. They prove banks can prioritize public purpose over private profit - a dangerous example that must be contained to Germany.

Islamic Banking: A Parallel Universe

While Western reformers struggled to create alternatives, the Islamic world built an entire parallel financial system based on different principles. Islamic banking, now a $2 trillion industry, proves that conventional banking isn’t the only way to intermediate capital.^[20]

Core principles include:

* No interest (riba): Money cannot generate money without real economic activity

* Risk sharing: Lender and borrower share profits and losses

* Asset backing: All financial transactions must involve real assets

* No speculation: Gambling and excessive uncertainty forbidden

* Ethical investment: No financing of alcohol, pork, weapons, etc.^[21]

Instead of interest-bearing loans, Islamic banks use:

* Murabaha: Bank buys asset, sells to customer at markup

* Musharaka: Joint venture with shared profits/losses

* Ijara: Leasing arrangements

* Sukuk: Asset-backed securities (not conventional bonds)^[22]

The 2008 crisis revealed Islamic banking’s strengths. While Western banks collapsed from trading fictional derivatives, Islamic banks remained stable - they could only finance real assets. While conventional banks needed bailouts, Islamic banks’ risk-sharing meant losses were distributed, not concentrated.^[23]

Yet Islamic banking faces constant pressure to conform to conventional models. The IMF and World Bank push for “harmonization” with global standards. Rating agencies penalize Islamic banks for not matching conventional metrics. Graduate programs teach Islamic finance as a quirky subspecialty, not a valid alternative.

The message is clear: you can have different banking, but not too different.

Modern Miracles: Banco Palmas and Community Currencies, 1998

In 1998, the Palmeira favela in Fortaleza, Brazil, faced a cruel irony. After residents spent 20 years building infrastructure - electricity, water, sewage - property values rose and gentrification began. The very people who’d improved the neighborhood couldn’t afford to stay.^[24]

Their solution was radical: create their own bank and currency. Banco Palmas would:

* Issue low-interest loans in local currency (“Palmas”)

* Provide credit without traditional collateral

* Keep money circulating locally

* Build community wealth, not extract it^[25]

The results:

* 93% of residents now shop locally (vs. 20% before)

* 1,800 businesses accept Palmas

* Thousands of jobs created

* Poverty rates plummeted

* The model spread to 113 Brazilian communities^[26]

The Brazilian central bank initially tried to shut Banco Palmas down. But unlike Depression-era experiments, Palmas had something new: international attention and academic support. Researchers documented its success. UN officials praised it. The central bank backed down, eventually partnering with community banks.

Similar successes worldwide:

* Ithaca HOURS (New York): $10 million in local trade over 20 years

* BerkShares (Massachusetts): 400 businesses, $140 million circulated

* Chiemgauer (Germany): €7 million annual volume, 600 businesses

* Bristol Pound (UK): Mayor takes salary in local currency^[27]

Each proves the same point: monetary diversity works. Communities with local currencies weather global shocks better. Small businesses thrive when money stays local. Unemployment falls when currency circulates rapidly.

Yet they all face the same constraints:

* Legal restrictions on currency issuance

* Tax complications requiring dual accounting

* Banking regulations limiting growth

* Media dismissal as “toy money”

* Academic ignorance of their successes

Why Alternatives Must Be Killed

The suppression of monetary alternatives isn’t irrational. From the perspective of existing power structures, it’s essential. Every successful alternative threatens core myths that justify the current system:

Myth 1: “Only experts can manage money”When Austrian mayors and Brazilian favela residents create better-functioning currencies, it exposes central banking as ideology, not science.

Myth 2: “There is no alternative”Margaret Thatcher’s famous phrase loses power when alternatives visibly work. If other systems are possible, current suffering is a choice.

Myth 3: “Private banking is efficient”When public banks like Sparkassen outperform private giants, it questions why banking profits should be private at all.

Myth 4: “Money must be scarce”When abundant local currency creates prosperity, it reveals that scarcity is engineered, not natural.

Myth 5: “Complexity requires centralization”When simple stamp scrip outperforms complex monetary policy, it suggests we don’t need central banks at all.

“It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.”

— Henry Ford

The tragedy of killed alternatives isn’t just lost prosperity. It’s lost knowledge. Each suppressed experiment contained lessons about how money could work differently. Each success proved that suffering isn’t inevitable - it’s policy.

The Phoenix Currencies

Yet alternatives keep arising. Like weeds through concrete, human creativity constantly sprouts new monetary forms:

* Timebanks: 500+ worldwide, trading hours instead of dollars

* LETS Systems: 1,500+ globally, facilitating non-monetary exchange

* Transition Currencies: 20+ towns creating resilient local economies

* Cryptocurrency: 20,000+ tokens challenging state monopolies

* Mutual Credit: Businesses trading without conventional money^[28]

Each generation rediscovers the same truths:

* Money is just an agreement

* Those agreements can be changed

* Better systems are possible

* Someone benefits from current dysfunction

* Change threatens those benefits

The digital age accelerates this rediscovery. Where Wörgl needed printing presses and stamp distributors, modern communities can launch currencies with smartphones. Where Depression-era experiments died in isolation, today’s alternatives network globally.

The question isn’t whether alternatives will emerge - they always do. The question is whether this time, enough people will understand what’s at stake to protect them.

Lessons from Money Martyrs

Every killed currency experiment teaches the same lessons:

* Success is more dangerous than failure: Failing experiments are ignored. Successful ones get destroyed.

* Legal systems protect monetary monopolies: Courts will always side with central banks against communities.

* Crisis creates opportunity: Alternatives emerge during breakdowns when official systems fail.

* Speed matters: The faster an alternative grows, the quicker it’s killed.

* Documentation is crucial: Suppressed experiments whose data survives inspire future attempts.

* Networks provide resilience: Isolated experiments die easily. Connected ones survive longer.

* Ideology matters more than mechanics: Alternatives fail not technically but politically.

The miracle of Wörgl wasn’t monetary - it was psychological. For one brief year, a community proved that prosperity was possible, that unemployment was unnecessary, that money could serve rather than rule. That knowledge, once gained, could never be fully suppressed.

Every alternative currency is a freedom movement. Every local monetary experiment is a declaration of independence. Every community that creates its own money rediscovers the same dangerous truth: we don’t need their system.

That’s why they must be killed.

That’s why we must keep creating them.

[This investigation concludes in Part 5: “Digital Chains or Digital Freedom: The Final Monetary Battle” - examining how the shift to digital currency represents either humanity’s final enslavement to financial control or its ultimate liberation.]

Footnotes

^[1]: Wörgl’s pre-experiment conditions: Muralt, Alexander von, “The Wörgl Experiment with Depreciating Money,” Annals of Public and Cooperative Economics, Vol. 10, No. 1 (1934), pp. 48-57.

^[2]: Unterguggenberger’s background: Schwarz, Fritz, Das Experiment von Wörgl (Verlang Genossenschaft, 1951), pp. 15-32.

^[3]: Gesell’s theory: Gesell, Silvio, The Natural Economic Order (1916), trans. Philip Pye (Peter Owen, 1958), Part III.

^[4]: The July 31, 1932 decision: Wörgl Municipal Archives, Council Minutes, July 31, 1932.

^[5]: Austrian National Bank lawsuit: Österreichische Nationalbank v. Gemeinde Wörgl, Austrian Supreme Court, September 1, 1933.

^[6]: Wörgl statistics: Fisher, Irving, Stamp Scrip (Adelphi, 1933), pp. 67-81.

^[7]: International attention: “The Wörgl Experiment,” The Economist, August 19, 1933, p. 346.

^[8]: Court ruling impact: Lietaer, Bernard, “The Wörgl Experiment: Post-Mortem,” International Journal of Community Currency Research, Vol. 19 (2015), pp. 32-41.

^[9]: Unterguggenberger’s death: Muralt, Wörgl Experiment, p. 89.

^[10]: Iowa experiments: Harper, Joel, “Scrip Money and Its Impact on Iowa Communities During the Great Depression,” Iowa Heritage Illustrated, Vol. 85, No. 2 (2004), pp. 56-67.

^[11]: Fisher’s calculations: Fisher, Irving, Booms and Depressions (Adelphi, 1932), Chapter 9.

^[12]: Roosevelt’s ban: Executive Order 6102, March 9, 1933; analyzed in Edwards, Sebastian, “The U.S. Ban on Private Gold Ownership,” NBER Working Paper No. 23123 (2017).

^[13]: Wära experiment: Godschalk, Hugo, “The Wära Free Money Experiment,” in Monetary Regionalisation, ed. J. Martignoni (Vdf Hochschulverlag, 2012), pp. 81-93.

^[14]: Alberta Social Credit: Finkel, Alvin, The Social Credit Phenomenon in Alberta (University of Toronto Press, 1989), pp. 45-78.

^[15]: Federal suppression: Reference re Alberta Statutes, [1938] S.C.R. 100, Supreme Court of Canada.

^[16]: French SEL systems: Laacher, Smain, “Les systèmes d’échange local,” Actes de la recherche en sciences sociales, Vol. 134 (2000), pp. 42-48.

^[17]: Sparkassen overview: Simpson, Christopher, “The German Sparkassen,” World Bank Policy Research Working Paper No. 5852 (2013).

^[18]: Public banking principles: Krahnen, Jan P., and Schmidt, Reinhard H., “On the Structure of the German Banking System,” Goethe University Working Paper (2004).

^[19]: Sparkassen statistics: DSGV (German Savings Banks Association), Annual Report 2020.

^[20]: Islamic banking size: Islamic Financial Services Board, Islamic Financial Services Industry Stability Report 2021.

^[21]: Islamic principles: Iqbal, Zamir, and Mirakhor, Abbas, An Introduction to Islamic Finance (Wiley, 2011), pp. 67-89.

^[22]: Islamic instruments: Ayub, Muhammad, Understanding Islamic Finance (Wiley, 2007), Chapters 7-11.

^[23]: Crisis performance: Hasan, Maher, and Dridi, Jemma, “The Effects of the Global Crisis on Islamic and Conventional Banks,” IMF Working Paper WP/10/201 (2010).

^[24]: Banco Palmas origins: Melo, Joaquim, and Magalhães, Sandra, Bancos Comunitários (Instituto Palmas, 2005), pp. 23-45.

^[25]: Palmas operations: Neiva, Augusto, et al., “Banco Palmas: Resistindo e Inovando,” Série Gestão Pública Vol. 1 (2013).

^[26]: Results and expansion: Meyer, Camille, “Community Currencies in Brazil,” International Journal of Community Currency Research, Vol. 17 (2013), pp. 32-38.

^[27]: Modern local currencies: Lietaer, Bernard, and Dunne, Jacqui, Rethinking Money (Berrett-Koehler, 2013), pp. 143-189.

^[28]: Alternative currency census: DeMeulenaere, Stephen, “2020 Annual Report of the Worldwide Database of Complementary Currency Systems,” International Journal of Community Currency Research, Vol. 24 (2020), pp. 30-53.