This is the second Monthly Outlook on Geopolitical Risk Assessment. December’s framework proved largely accurate on Ukraine: settlement negotiations advanced further than baseline projected, with 90% of the 20-point peace plan now agreed and US security guarantees documented in writing.[^1] However, the Maduro capture was not anticipated and represents a paradigm shift in US willingness to use military force for regime change in the Western Hemisphere. Three additional crisis vectors also emerged: Iran protests threatening regime stability, Saudi-UAE military confrontation in Yemen, and Federal Reserve banking stress signals.This Monthly Outlook & Weekly Update is available for Founding Members subscribers at $1,188/year ($99/month). Opens to free subscribers next month.TATSU GEOPOL is the same geopolitical intelligence Wall Street pays Stratfor and Eurasia Group $40k/year for - delivered at real-time speed, for 3% the cost!

Phase 1: Analytical Framework

Major Strategic Shifts Identified

* US Captures Venezuelan President Maduro - First military seizure of sitting head of state since Noriega 1989; Venezuela under martial law[^30]

* Ukraine Settlement Framework at 90% - Security guarantees in writing, only territory and NPP remain unresolved[^1]

* Iran Protests Erupting - Deadly clashes in multiple cities, Trump threatening intervention, regime stability in question[^2]

* Saudi-UAE Yemen Fracture - Two GCC allies now conducting military operations against each other’s proxy forces[^3]

* Bulgaria Joins Eurozone - Counter-signal to European fracture narrative; ECB institutional power growing[^4]

* Democratic Opposition to Settlement - Philip Gordon organizing resistance; Congressional ratification now uncertain[^5]

* Fed Banking Stress - $74.6B+ REPO injections signal underlying liquidity concerns[^6]

* Israel-Somaliland Recognition - First UN member state recognition creates Horn fragmentation precedent[^7]

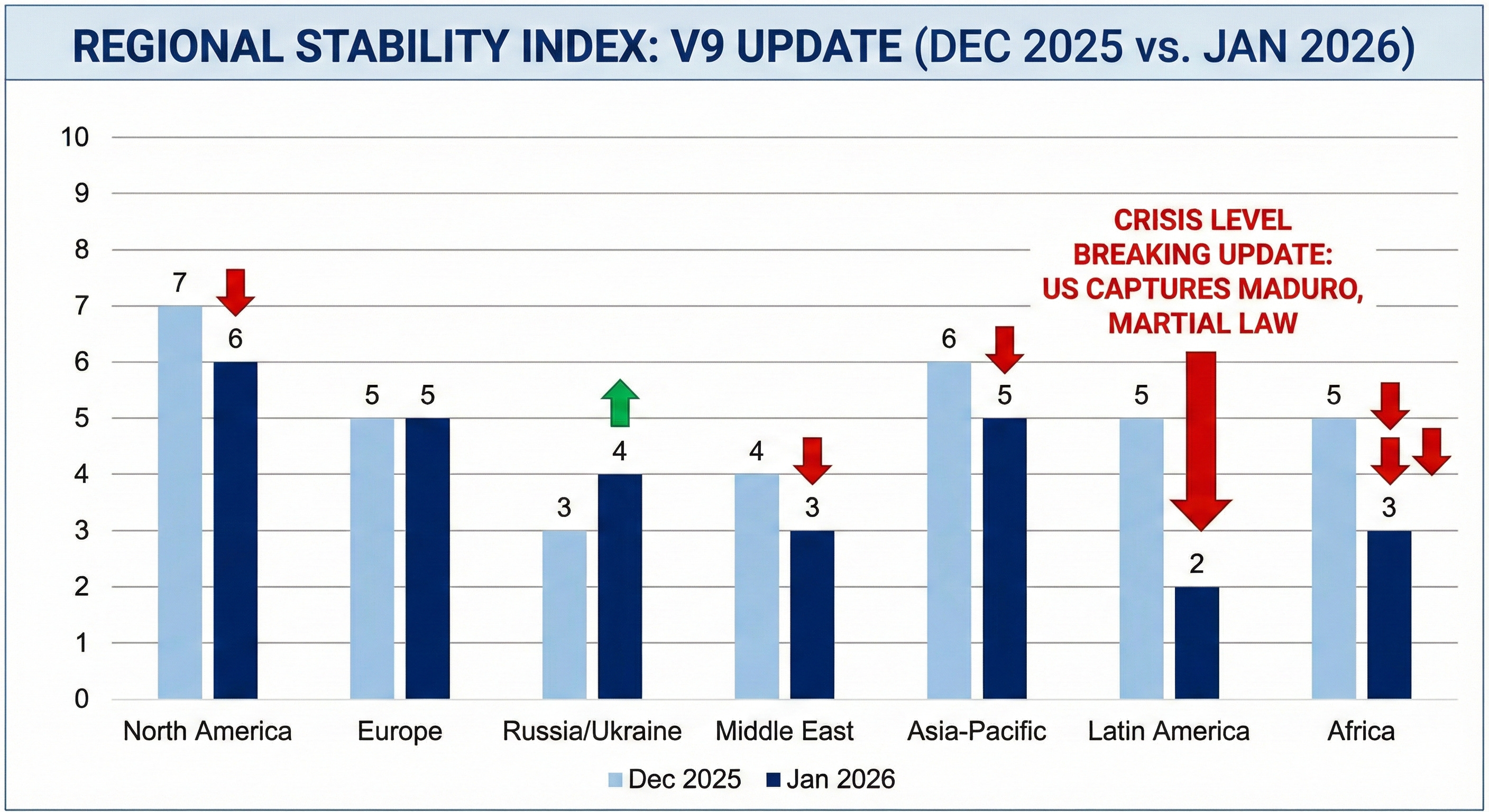

Regional Stability Rankings

[CHART: Regional Stability Index V9 Update - Dual bar chart comparing December 2025 vs January 2026 scores, with Latin America highlighted in red showing dramatic 5→2 collapse. Include arrow annotations for major changes.]

Risk Event Categories for January

* Venezuela regime transition aftermath — military mobilization, oil infrastructure, regional response

* Iran protest escalation or regime crackdown

* Kremlin acceptance or rejection of 20-point plan

* Saudi-UAE Yemen de-escalation or expansion

* Settlement framework completion or collapse

* Congressional security guarantee signals

* Fed REPO intervention pattern

Market Implication Themes

* Oil majors: Chevron +6.7% on Maduro capture; Venezuelan production access in play

* Defense sector: Settlement headwinds vs. Iran/Asia/LatAm demand

* Energy: Venezuela + Iran supply dynamics; production uncertainty

* EUR: Settlement benefit vs. coalition fracture

* Gold: Safe haven on Venezuela crisis + Middle East + Fed stress

* Gulf sovereigns: Saudi-UAE fracture introduces new risk

* LatAm equities: Contagion risk from Venezuela instability

Phase 2: Executive Summary

Bottom Line

The capture of Venezuelan President Nicolás Maduro by US special operations forces on January 4-5 represents the most significant unilateral US military action in Latin America since the 1989 Panama invasion. This operation—executed without Congressional authorization, UN mandate, or coalition support—signals a fundamental shift in Trump administration willingness to use military force for regime change. Venezuela is now under martial law with oil infrastructure under military control.[^31]

The Ukraine settlement framework remains at 90% completion with security guarantees in writing.[^1] However, the Maduro operation raises questions about US strategic priorities and bandwidth. Regional allies (Brazil, Colombia, Mexico) have condemned the action, potentially complicating hemispheric cooperation.

Four concurrent crises now demand attention:

* Venezuela regime transition: Martial law declared, military mobilization, oil production uncertain. UN Security Council emergency session. Only 33% US public approval.[^34]

* Iran protests have erupted across multiple cities with fatalities. Trump threatening intervention (“locked and loaded”).[^2] Question: Does Maduro capture signal pattern for Iran?

* Saudi Arabia and UAE conducting military operations against each other’s proxies in Yemen.[^3] Most serious GCC internal confrontation since 2017 Qatar crisis.

* Federal Reserve continues emergency liquidity injections ($74.6B+ via REPO), signaling underlying banking system stress.[^6]

Settlement Probability: 75-80% within 90 days (slight downgrade due to US attention on Venezuela)

Overall Risk Posture: SEVERELY ELEVATED. Latin America crisis-level (2/10). Middle East/Africa deteriorating. Russia/Ukraine improving but may face attention competition.

Key Strategic Signals

1. US Captures Venezuelan President in Military Operation (Confidence: 100%)

[CHART: Venezuela Operation Map - Map of Venezuela showing Caracas (capture location), oil infrastructure zones, military bases, and arrows indicating US operation. Includes inset showing NYC courthouse location.]

US special operations forces captured President Nicolás Maduro and First Lady Cilia Flores in Caracas on January 4-5, 2026.[^30] Both appeared in federal court in New York facing narco-terrorism charges. Defense Secretary Hegseth stated “Maduro didn’t know they were coming until three minutes before they arrived.”[^35] This is the first US military capture of a sitting head of state since Manuel Noriega in 1989. Venezuela has declared martial law and full military mobilization, placing oil and key industries under temporary military control.[^31] ECOWAS condemned the action as a violation of sovereignty.[^36] Chevron shares rose 6.7% on market open; an unknown investor earned $400,000 betting on Maduro’s fall on futures markets (per WSJ).[^37]

2. Settlement Framework at Critical Stage (Confidence: 85%)

The December 28 Mar-a-Lago meeting produced the most advanced peace framework since Russia’s invasion. Zelensky confirmed “90% agreed” with only territorial boundaries and Zaporizhzhia NPP control remaining.[^1] Security guarantees are documented—a 15-year US commitment requiring Congressional ratification. Risk: Venezuela operation may consume US bandwidth and complicate European ally coordination.

3. Iran Protests Threaten Regime (Confidence: 75%)

Beginning late December and intensifying through New Year, protests have erupted in Hamedan, Tehran, and other cities.[^2] What started as economic grievances over the rial’s collapse has evolved into broader anti-regime demonstrations.[^8] Trump’s response (“US ready to fight for protesters”) represents explicit regime change signaling.[^9] Critical question: Does the Maduro operation establish a pattern for Iran intervention?

4. Saudi-UAE Alliance Fracturing (Confidence: 80%)

The UAE announced termination of remaining “counter-terrorism” teams in Yemen.[^3] More significantly, Saudi-backed forces launched “Operation Camps Handover” with Saudi airstrikes killing 7 UAE-backed STC forces.[^11] This represents the most serious GCC internal confrontation since the 2017 Qatar crisis.

5. Democratic Opposition to Settlement Emerges (Confidence: 70%)

Former Harris advisor Philip Gordon is urging Zelensky to reject the framework, arguing Trump’s Article 5-equivalent guarantee “will not be implemented.”[^5] This creates new Congressional variable: ratification may face bipartisan opposition from isolationist Republicans AND interventionist Democrats.

6. Bulgaria Eurozone Entry (Confidence: 95%)

Bulgaria became the 21st eurozone member on January 1.[^4] This counter-signals December’s European fracture narrative—the EU can simultaneously fail on Ukraine coordination while succeeding on monetary integration.

Risk Posture Assessment

Current risk levels are SEVERELY ELEVATED with Latin America now in active crisis. Latin America has collapsed from 5/10 to 2/10 on the Maduro capture and Venezuelan martial law—the largest single-month decline in any region. Russia/Ukraine has improved from 3/10 to 4/10 on framework progress. Middle East has deteriorated from 4/10 to 3/10 on Iran protests and Yemen fracture. Africa remains severely stressed at 3/10 on Sudan genocide and Sahel coups.

The 30-day window carries extreme uncertainty. Primary risk driver: Venezuela transition could absorb US attention and resources, potentially delaying settlement finalization and emboldening adversaries who perceive US overextension.

Phase 3: Strategic Shifts - Deep Analysis

1. US Military Capture of Venezuelan President Maduro

Confidence: 100% | Impact: Extreme | Timeframe: Immediate

Current Status

On January 4-5, 2026, US special operations forces executed a military operation in Caracas that resulted in the capture of Venezuelan President Nicolás Maduro and First Lady Cilia Flores.[^30] Both were transported to New York City, where they appeared before a federal judge on narco-terrorism charges. Maduro rejected all drug-related allegations, asserting his legitimacy as Venezuela’s elected president. Cilia Flores appeared with visible injuries—a bandage on her forehead and bruising near her right eye.[^38]

Defense Secretary Pete Hegseth stated: “Maduro didn’t know they were coming until three minutes before they arrived.”[^35] This represents the first US military capture of a sitting head of state since the 1989 Panama invasion that seized Manuel Noriega.

Immediate Aftermath

Venezuela has declared:

* Full military mobilization of armed forces

* Martial law for oil industry and key infrastructure employees

* Oil and strategic industries under temporary military control[^31]

International response has been swift and largely critical:

* UN Security Council convened emergency session; Russia condemned the action as a “crime”[^32]

* ECOWAS called for respect of Venezuela’s sovereignty[^36]

* Mass protests erupted in New York (outside courthouse) and London

* Brazil, Colombia, and Mexico have reportedly condemned the action

Strategic Analysis

This operation signals a fundamental shift in US foreign policy under Trump’s second term:

* Monroe Doctrine Revival: The operation represents the most aggressive assertion of US hemispheric dominance since the Cold War. The apparent justification—narco-terrorism charges—provides legal cover for what is effectively regime change.

* Precedent for Iran?: Coming days after Trump’s “locked and loaded” rhetoric on Iran protests, the Maduro capture raises questions about whether this represents a pattern. The administration has demonstrated willingness to act unilaterally against adversarial regimes.

* Oil Calculus: Chevron’s 6.7% stock surge suggests markets anticipate improved access to Venezuelan oil reserves—the world’s largest proven reserves. An investor made $400,000 on futures betting on Maduro’s fall (per WSJ).[^37]

* Domestic Politics: Only 33% of Americans approve of the operation per Reuters/Ipsos.[^34] This may constrain further military adventures but has not deterred the administration.

Trajectory Assessment

* 7-day outlook: Power vacuum in Caracas. Military council likely to assume control. Oil production disruption probable. Regional condemnation but no military response. Confidence: 80%

* 30-day outlook: Transition government formation or continued military rule. US recognition of opposition figure possible. Oil production 20-40% below normal. Confidence: 65%

* 90-day outlook: Three scenarios emerge (see below). Settlement framework for new elections or prolonged instability. Confidence: 50%

Probability Pathways

[CHART: Venezuela Transition Scenario Decision Tree - Flowchart showing four pathways from “Maduro Captured” node: Managed Transition (35%), Prolonged Instability (40%), Regional Contagion (15%), International Isolation (10%), with key trigger conditions and market impacts for each branch]

Market Implications

* Chevron (CVX): Already +6.7%. Further upside if transition is orderly; downside if production disrupted.

* Oil: Venezuelan production (~800k bpd) at risk. Net bullish on supply disruption.

* LatAm Equities: Contagion risk to Brazil, Colombia. Avoid broad exposure.

* Defense: US military contractors may see increased demand for regional operations.

* Gold: Safe haven bid on geopolitical uncertainty.

[CHART: Venezuela Oil Production Scenarios - Line chart showing three production trajectories from Jan 2026 baseline (~800k bpd): Managed Transition (recovery to 900k by Q3), Prolonged Instability (drop to 400k), Regional Contagion (collapse to 200k). Include historical context 2019-2025.]

[CHART: Chevron Stock Reaction - Candlestick chart showing CVX price action Jan 3-5, with +6.7% spike annotated. Include volume bars and comparison to XLE (energy sector ETF).]

Recommended Positioning

* Maintain zero Venezuelan asset exposure

* Reduce broad LatAm equity exposure by 25%

* Consider oil call spreads (60-day) for supply disruption

* Add gold as geopolitical hedge (+2%)

2. Ukraine Settlement Framework

Confidence: 85% | Impact: Very High | Timeframe: 30-90 days

Current Status

The 20-point peace plan is now 90% agreed according to Zelensky’s New Year address:[^1]

Component Status Notes:

The remaining 10% represents the hardest issues. Russia demands recognition of all annexed territories plus Crimea and NATO exclusion. Ukraine offers current contact line with referenda after 60-day ceasefire. Russia rejected the ceasefire proposal entirely.[^13]

Strategic Analysis

Four pathways exist for January:

Pathway A: Framework Completion (35% probability)

Washington summit produces breakthrough on territory. This requires one of:

* Russia accepts something less than full territorial demands (current contact line + Crimea recognition)

* Ukraine accepts formal recognition of Russian control beyond current line

* Creative solution emerges (phased processes, international administration, ambiguous status formulas)

Historical precedent supports creative solutions: Åland Islands, Hong Kong handover, various EU compromises demonstrate that “unbridgeable” gaps can be finessed with sufficient political will. Trump’s deal-making style may favor such approaches.

Key tell: If Kremlin response before summit includes specific counter-proposals rather than general rejection, completion probability rises to 45%.

Pathway B: Extended Impasse (40% probability)

The 10% gap proves unbridgeable in January but negotiations continue. This is the “muddle through” scenario where:

* Framework remains at 90%

* Military operations continue at moderate intensity

* Settlement advances to February/March timeline

* Spring offensive window creates eventual forcing function

This pathway is most likely if Kremlin maintains current posture: praise the process, reject specifics, continue military pressure.

Key tell: Kremlin response that restates existing demands without movement but maintains diplomatic engagement.

Pathway C: Collapse (15% probability)

Kremlin rejection or maximalist counter-demands end negotiations. This triggers:

* Spring offensive preparations accelerate

* Settlement probability drops to 40-50%

* Defense sector rallies, EUR weakens

* Energy spikes on extended conflict expectations

Key tell: Kremlin response that includes impossible demands (full NATO withdrawal from Eastern Europe, sanctions removal preconditions) or outright rejection.

Pathway D: US Distraction (10% probability)

Iran crisis escalates, pulling US attention from Ukraine. This could manifest as:

* US military action against Iran

* Major diplomatic crisis requiring White House focus

* Congressional attention shifts to Iran authorization debates

Under this scenario, settlement momentum stalls regardless of Russian posture. Framework completion probability drops to 30% as negotiations lose urgency.

Key tell: Trump administration Iran rhetoric escalating from current “locked and loaded” to specific military threats or actions.

Trajectory Assessment

* 7-day outlook: Kremlin response expected before Washington summit. 70% probability of response by January 10.

* 14-day outlook: Washington summit determines January trajectory. Framework signing or extended impasse becomes clear.

* 30-day outlook: If no January signing, February becomes implementation month or spring offensive preparation begins.

Market Implications

2. Iran Protests - New Crisis Vector

Confidence: 75% | Impact: High | Timeframe: Immediate

Current Status

Protests have erupted across multiple Iranian cities beginning late December:[^2]

* Hamedan: Deadliest clashes—protesters burning Qurans and prayer books, security forces responding with force, multiple fatalities[^8]

* Tehran: Student involvement expanding protest base beyond initial merchant/economic grievances[^14]

* Other cities: Geographic spread continuing but not yet nationwide

The protests began as economic grievances over the rial’s collapse but have evolved into broader anti-regime demonstrations with religious dimensions. The Quran burnings in Hamedan represent significant escalation—attacking religious symbols strikes at the Islamic Republic’s foundational legitimacy.

Trump Administration Response

The administration has escalated rhetoric dramatically:[^9]

* “The US is ready to fight for the protesters”

* “Locked and loaded” threatening intervention if Iran “continues to shoot and kill”

* Increased US satellite/ISR activity over Iran detected[^10]

This represents explicit regime change signaling—the most aggressive US posture toward Iran since the Trump 1.0 administration. The rhetoric goes beyond sanctions threats to imply potential military action.

Netanyahu’s Mar-a-Lago Presence

Netanyahu spent New Year’s Eve at Mar-a-Lago, meeting with Trump and Christian Zionist leaders.[^15] This suggests active US-Israel coordination on Iran policy. Combined with increased satellite activity, the diplomatic signaling indicates serious consideration of Iran options.

Iran’s Response

Iranian officials have pushed back sharply:

* Supreme Leader Khamenei: Iran in “full-fledged war with US, Israel, Europe”[^16]

* Defense Minister: “Iran’s missile strength cannot be destroyed, neither by bombs nor by drones”

* FARAJA (National Police): Warnings about “terrorist rioters”

* Counter-protests organized by regime supporters

Strategic Analysis

This is the most significant Iran development since the 2022 Mahsa Amini protests. The convergence of factors is concerning:

* Internal instability: Protests spreading, students joining, religious dimensions emerging

* External pressure: Trump rhetoric, satellite activity, Netanyahu coordination

* Regional isolation: Syria fell to HTS (Iranian ally lost), Hezbollah weakened by ceasefire

* Economic collapse: Rial in free fall, sanctions pressure continuing

Four scenarios for Iran trajectory:

Scenario A: Regime Crackdown Success (40% probability)Iran deploys IRGC/Basij forces, crushes protests with force, arrests leaders. Short-term stability restored but underlying grievances remain. International condemnation but no military response.

Scenario B: Protests Fizzle (25% probability)Economic concessions or protest fatigue leads to dissipation. Regime survives without major crackdown. Status quo ante restored.

Scenario C: Sustained Unrest (25% probability)Protests continue at moderate intensity for weeks/months. Regime under pressure but stable. Creates ongoing uncertainty for markets and regional dynamics.

Scenario D: US Military Action (10% probability)Trump follows through on rhetoric. US strikes Iranian military/nuclear facilities. Major regional escalation. Oil spikes $20-30.

Connection to other theses: Iran instability affects:

* Israel-Hezbollah: Reduced Iranian capacity to support proxies, but regime under pressure might accelerate external operations as distraction

* Yemen: Houthi backing uncertain if Iran focused internally

* Ukraine settlement: US attention may shift, potentially stalling framework momentum

Market Implications

* Oil: Add $5-10 Iran supply risk premium (Scenario D: +$20-30)

* Gold: Safe haven bid on Middle East instability (+3-5% base case, +10% escalation)

* Defense: Israeli names (Elbit) benefit from escalation hedge

* Shipping: Red Sea/Strait of Hormuz risk premium if escalation

3. Saudi-UAE Yemen Fracture

Confidence: 80% | Impact: Medium-High | Timeframe: Immediate

Current Status

The UAE Ministry of Defense announced termination of remaining “counter-terrorism” teams in Yemen, formally ending Emirati military presence.[^3] This follows years of gradual drawdown but represents formal conclusion of UAE’s Yemen intervention.

More significantly, Saudi Arabia and UAE-backed forces have turned on each other:[^11]

* Saudi-backed “Homeland Shield Forces” launched “Operation Camps Handover”

* Saudi airstrikes killed 7 UAE-backed Southern Transitional Council (STC) forces

* Flights from Aden airport halted amid tensions

* Hadhramaut province becoming contested zone

The Guardian characterized tensions as reaching “boiling point.”[^17]

Strategic Analysis

This is extraordinary: two GCC allies, ostensibly partners in the Yemen intervention since 2015, are now conducting military operations against each other’s proxy forces. This represents the most serious GCC internal confrontation since the 2017 Qatar crisis.

Underlying causes of Saudi-UAE divergence:

* Strategic priorities: UAE pivoting toward economic diversification (tourism, tech, finance), reducing regional military commitments. Saudi Arabia remains focused on regional security competition with Iran.

* Yemen objectives: UAE backed southern separatists (STC) seeking independent South Yemen. Saudi Arabia backs unified Yemen under Hadi government successor. These goals are incompatible.

* Iran approach: UAE has engaged in quiet diplomacy with Tehran. Saudi Arabia maintains hardline opposition.

* Israel relations: Both normalized via Abraham Accords framework, but UAE moved faster and deeper.

Implications:

1. Red Sea SecurityUAE withdrawal affects Bab el-Mandeb chokepoint security. With Houthis controlling much of northern Yemen and conducting Red Sea attacks on shipping, the power vacuum in southern Yemen creates additional risk to maritime commerce.

2. Israel’s Somaliland CalculationIsrael’s December 26 recognition of Somaliland—providing alternative Red Sea port access via Berbera—now appears prescient.[^7] If Yemen instability spreads and Bab el-Mandeb becomes more contested, the Somaliland route gains strategic value.

3. Houthi OpportunityInternal fighting among anti-Houthi forces creates opportunity for Houthi advances. This could expand Iranian-aligned territorial control despite Iran’s internal troubles—a paradox where Iran gains regional influence while facing domestic instability.

4. GCC Architecture StressIf Saudi-UAE confrontation escalates, the entire Gulf security architecture built on GCC coordination faces fundamental challenge. This affects US alliance management, energy market stability, and regional power balance.

Market Implications

* Gulf sovereigns: Saudi-UAE fracture introduces new risk to regional stability assumptions. Credit spreads may widen.

* Oil: Yemen instability affects Red Sea shipping routes. Brent +$2-3 risk premium.

* Shipping: Container rates face pressure from Bab el-Mandeb concerns.

* Defense: Gulf defense spending may increase as allies hedge against each other.

4. Bulgaria Eurozone Entry

Confidence: 95% | Impact: Medium | Timeframe: Completed

Current Status

Bulgaria became the 21st eurozone member on January 1, 2026:[^4]

* Exchange rate fixed at 1.95583 lev = €1

* Bulgarian National Bank Governor joins ECB Governing Council

* Eurozone now covers 350+ million Europeans

* 49% of Bulgarians opposed adoption[^12]

Christine Lagarde statement: “I warmly welcome Bulgaria to the euro family… The euro is a powerful symbol of what Europe can achieve when we work together, and of the shared values and collective strength that we can leverage to confront the global geopolitical uncertainty that we face at the moment.”[^4]

Strategic Analysis

This is a counter-signal to December’s European fracture narrative.

December showed fracture:

* Belgium blocking €140B Ukraine loan

* Italy delaying military aid decree

* Hungary/Slovakia maintaining pro-Russia positions

* EU summit failure on Russian assets

January shows consolidation:

* Eurozone expanding despite external pressure

* ECB institutional power growing

* Monetary integration continuing

Interpretation: Europe is fracturing on security policy while consolidating on monetary integration. These are different dynamics—the EU can simultaneously fail on Ukraine coordination while succeeding on currency union expansion.

EU Governance Critique

The euro adoption was driven by Brussels institutions rather than Bulgarian popular mandate (49% opposed). This pattern—technocratic expansion over democratic hesitation—remains the EU’s core tension. Lagarde and von der Leyen continue accumulating institutional power while member state populations express reservations.

The 2026 dynamic: unelected Brussels officials (Lagarde at ECB, von der Leyen at Commission) drive integration over national democratic processes. This creates legitimacy tensions that may eventually constrain further integration—but for now, institutional momentum continues.

Market Implications

* EUR: Modestly strengthened by expansion signal (+0.3-0.5%)

* Bulgarian assets: Now euro-denominated, reduced currency risk

* Eastern European convergence: Romania next candidate, creating investment thesis

* Inflation watch: Merchant price rounding typically adds 0.5-1% to CPI in adoption year

5. Democratic Opposition to Settlement

Confidence: 70% | Impact: Medium-High | Timeframe: 30-90 days

Current Status

Former Harris advisor Philip Gordon is publicly urging Zelensky to reject the framework:[^5]

“The essence of the proposed deal, it seems, is that Ukraine will give up territory in the disputed Donbass region in exchange for reliable security guarantees from the US… [but] Trump’s guarantees will not be implemented.”

This represents the first organized Democratic establishment opposition to the settlement process. Gordon’s argument: Trump’s commitments cannot be trusted because future administrations (including potentially Democratic ones) will not honor them.

Strategic Analysis

Congressional dynamics now face cross-cutting pressures:

Opposition coalition forming:

* Isolationist Republicans (Rand Paul wing) opposing any foreign commitments

* Interventionist Democrats (Gordon wing) viewing terms as “rewarding Russian aggression”

* Ukraine hawks in both parties opposing territorial concessions

* Human rights advocates opposing legitimization of occupation

Support coalition:

* Trump loyalist Republicans supporting presidential initiative

* Pragmatist Democrats prioritizing war termination

* Business interests seeking sanctions relief and reconstruction opportunities

* War-weary public (polling shows majority support settlement)

The 15-year security guarantee requires Congressional approval—likely 67 Senate votes for treaty ratification. This is achievable with bipartisan support but vulnerable to organized opposition from either flank.

Trajectory Assessment

* If framework terms remain as currently reported, ratification faces 60-65% probability

* If terms seen as more Ukraine-favorable than expected, probability rises to 75%

* If terms seen as “Putin victory,” probability drops to 40%

Market Implications

* Congressional rejection risk: Settlement unravels, all positioning reverses

* Approval signals: Ukrainian debt rallies, settlement durability confirmed

* Uncertainty premium persists until ratification clarity (expect 60-90 day timeline after signing)

6. Federal Reserve Banking Stress

Confidence: 70% | Impact: Medium | Timeframe: Ongoing

Current Status

The Federal Reserve continues emergency liquidity operations:[^6]

* $31B single REPO injection reported January 1-2

* $74.6B+ cumulative recent REPO activity

* Pattern suggests ongoing banking system stress

What REPO Operations Signal

REPO (Repurchase Agreement) operations provide short-term liquidity to banks facing funding pressures. The Fed accepts Treasury securities as collateral and provides cash. Sustained large-scale REPO activity indicates:

* Year-end balance sheet pressures: Banks managing regulatory capital requirements create temporary funding gaps

* Underlying liquidity stress: System not self-funding smoothly through interbank markets

* Fed as continuous lender of last resort: Intervention required to maintain market functioning

Historical Context

The September 2019 REPO crisis required $75B+ daily Fed interventions and presaged the March 2020 market stress. Current patterns are not at 2019 levels but warrant monitoring.

Geopolitical Connection

Financial system stress constrains policy options:

* Limits appetite for aggressive sanctions enforcement that might destabilize markets

* Creates domestic economic vulnerability that affects risk tolerance

* May influence settlement urgency (end geopolitical uncertainty to reduce financial stress)

* Could constrain Iran confrontation options if markets are fragile

This is typically excluded from geopolitical analysis but represents background condition affecting all US foreign policy decisions.

Market Implications

* Equity volatility: Banking stress creates risk-off potential

* Gold: Safe haven on financial system concerns

* Policy constraints: Aggressive foreign policy may face domestic limits

* Fed communication: Watch for signals about REPO facility expansion or standing facility changes

7. Military Operations During Negotiations

Confidence: 85% | Impact: Medium-High | Timeframe: Ongoing

Current Status

Russia rejected ceasefire proposals, maintaining military pressure during negotiations:[^13]

* 205-drone New Year attack: Largest single drone assault of 2026[^18]

* 9 settlements captured: Russian advances continue in Donbas

* Odessa “semi-blockade”: WSJ reports economic stranglehold tightening[^19]

* Kherson café attack: 27 civilians killed on New Year’s Eve[^20]

* Putin reserve mobilization: Decree authorizing call-up for infrastructure protection[^21]

Strategic Analysis

Russia’s military pressure during negotiations serves multiple purposes:

* Demonstrate alternative: Show continued operations produce results if talks fail

* Improve position: Each territorial gain strengthens negotiating leverage

* Test resolve: Gauge whether Ukraine/West will concede to stop attacks

* Domestic signaling: Show Russian public military option remains viable

* Create urgency: Pressure Ukraine to accept terms before further losses

The 10:1 Russian drone advantage remains structural. Ukraine cannot reverse this disadvantage through current force generation, creating incentive for negotiated settlement rather than continued attrition.

Oreshnik Deployment

Russia’s nuclear-capable Oreshnik hypersonic missile system has entered “active service” according to Defense News.[^22] Deployment during peace talks signals escalation in capability while negotiating—a classic pressure tactic but also genuine military advancement.

Market Implications

* Continued operations: Energy elevated, defense supported

* Operational slowdown: Energy softens, defense faces headwinds

* Major escalation: Energy spikes, defense surges

Phase 4: Alternative Scenarios & Tail Risks

Primary Thesis Summary

The base case anticipates 78-82% probability of negotiated settlement framework within 90 days, with 35-40% probability of signed framework in January specifically. This is supported by unprecedented framework progress (90% agreed), documented security guarantees, and active Trump engagement. The primary risks are Kremlin maximalism on territory, Congressional ratification uncertainty, and potential distraction from Iran crisis.

Alternative Scenario: The Contrarian Case

What if we’re wrong?

Iran could derail everything. If protests escalate and Trump follows through on intervention threats, US attention shifts from Ukraine to Middle East. Settlement momentum stalls. Russia exploits distraction to improve military position. Framework collapses not from Kremlin rejection but from US disengagement.

Under this scenario:

* Settlement probability drops to 40-50%

* European defense outperforms as conflict extends

* Energy spikes on dual crisis (Ukraine + Iran)

* Gold rallies on safe haven demand

* EUR weakens on extended European security uncertainty

The 90% agreed figure may be misleading. The easy issues are agreed; the hard issues remain. Security guarantees and military arrangements matter little if territorial boundaries cannot be resolved. Historical precedent (Minsk I, Minsk II, Istanbul 2022) shows frameworks can be 90% complete and still collapse on the remaining 10%. Every previous Ukraine negotiation has failed on territory.

Democratic opposition may be more significant than assessed. If Philip Gordon represents broader Democratic establishment view rather than isolated voice, Congressional ratification faces serious opposition. The guarantee requires 67 Senate votes—a high bar with organized opposition from both flanks. Democratic opposition could prevent ratification even if Trump delivers Russian agreement.

Saudi-UAE fracture may spread. If Yemen confrontation escalates beyond proxy fighting to direct Saudi-UAE tensions, the entire Gulf security architecture faces stress. This could affect:

* Energy market stability (GCC production coordination)

* US alliance management (choosing sides)

* Regional conflict dynamics (multiple simultaneous crises)

Black Swan Triggers

Events that could fundamentally alter assessments:

* Russian tactical nuclear demonstration: Settlement collapses, NATO mobilization, global crisis

* Iranian nuclear breakout announcement: US/Israel military action, regional war

* Putin health crisis: Succession uncertainty, potential policy discontinuity

* Major Ukrainian strike on Russian strategic infrastructure: Escalation spiral

* Chinese Taiwan blockade announcement: Global crisis overshadowing all else

* US banking crisis: Policy paralysis, risk-off across all assets

Scenario Probability Assessment

Scenario Probability Key Driver Settlement framework signed January 35% Washington summit success Negotiations continue, no January signing 40% Territorial impasse Negotiations collapse 15% Kremlin rejection US distracted by Iran 10% Protest escalation → intervention

Portfolio Implications of Being Wrong

If contrarian case materializes (collapse or extended impasse):

If Iran escalation scenario (10% probability):

Phase 5: Regional Assessments

North America

Stability Index: 7/10 (— unchanged vs. December)

Key Developments

* Settlement Diplomacy Leadership: Trump administration assumes primary responsibility for Ukraine negotiations. December 28 Mar-a-Lago meeting and scheduled Washington summit demonstrate sustained engagement.[^1] US positioned as indispensable broker but also owns outcomes.

* Domestic Policy Continuity: Economic deregulation, immigration enforcement, energy policy proceed on parallel track. No significant domestic instability affecting foreign policy capacity.

* Congressional Dynamics: Security guarantee’s Congressional approval requirement introduces new variable. Democratic opposition organizing (Philip Gordon).[^5] Ratification politics will affect settlement durability.

* Fed Banking Stress: $74.6B+ REPO injections signal underlying liquidity stress.[^6] This constrains aggressive foreign policy options and may influence settlement urgency.

* Iran Policy Escalation: Trump’s “locked and loaded” rhetoric toward Iran represents most aggressive US posture since Trump 1.0 administration.[^9] May compete with settlement for attention.

Outlook Assessment

* 30-day: Washington summit dominates. 80% confidence in stability maintenance.

* 60-day: Congressional consideration begins if framework signed. 75% confidence.

* 90-day: Ratification outcome shapes durability. 70% confidence.

Investment Considerations: US equities maintain safe-haven status. Dollar strength persists on rate differentials. Defense (US names) less exposed to Ukraine settlement than European counterparts given Indo-Pacific and Middle East demand drivers.

Europe

Stability Index: 5/10 (— unchanged vs. December)

Key Developments

* Coalition Fracture Confirmed: December EU summit failure on Russian assets. Belgium’s €140B loan block, Italy’s aid delay demonstrate structural disagreements persist.

* Bulgaria Joins Eurozone: Counter-signal—21st member as of January 1.[^4] ECB institutional power growing even as security coalition fragments.

* Defense Spending Acceleration: Poland 4.7% GDP target (NATO’s top spender). Estonia first to exceed 5%. EU ReArm Europe: €150B SAFE fund, €800B leverage to 2029.

* Washington Summit: European leaders invited but arrive without unified position on territorial compromise or burden-sharing. Summit may expose divisions rather than resolve them.

* UK Defense Delay: Starmer delayed Defence Investment Plan over “affordability”[^23]—rhetoric vs. reality gap widening.

Outlook Assessment

* 30-day: Washington summit determines trajectory. 55% confidence in stability.

* 60-day: Post-summit implementation or recrimination. 50% confidence.

* 90-day: Electoral calendars affect policy continuity. 50% confidence.

Investment Considerations: European defense faces binary January outcome but structural support from 5% target. Rheinmetall most Ukraine-exposed; BAE, Thales more diversified. EUR faces settlement/collapse binary—maintain 5-7% CHF hedge. Italian exposure (Leonardo) carries political risk premium.

Russia/Ukraine

Stability Index: 4/10 (▲ +1 vs. December)

Key Developments

* Framework at 90% Completion: Security guarantees documented, military arrangements agreed.[^1] Only territorial and NPP issues remain. Qualitative change in conflict trajectory.

* Kremlin Response Pending: Russia has not formally responded to 20-point plan, stating it is “formulating response.”[^13] Response expected before Washington summit.

* Military Operations Continue: 205-drone New Year attack,[^18] 9 settlements captured, Odessa semi-blockade,[^19] Kherson café attack (27 dead).[^20]

* Putin Reserve Mobilization: Decree authorizing call-up for infrastructure protection[^21]—suggests concerns about Ukrainian deep-strike capabilities.

* Democratic Opposition: Philip Gordon urging Zelensky to reject[^5]—new variable in settlement dynamics.

Outlook Assessment

* 30-day: Kremlin response and summit determine trajectory. 60% confidence in stability at current level.

* 60-day: Implementation negotiations or extended impasse. 50% confidence.

* 90-day: Spring offensive window creates deadline. 45% confidence.

Investment Considerations: Ukrainian sovereign debt highly speculative but potentially +20-30% if settlement signed. Eastern European sovereigns benefit from reduced proximity risk. Russian assets remain sanctioned and uninvestable. Avoid directional exposure; use options for volatility participation.

Middle East

Stability Index: 3/10 (▼ -1 vs. December) — MOST SIGNIFICANT DETERIORATION

Key Developments

* Iran Protests Erupting: Deadly clashes in Hamedan,[^8] students joining,[^14] geographic spread. Most significant since 2022 Mahsa Amini protests. Trump threatening intervention.[^9]

* Saudi-UAE Yemen Fracture: UAE withdrawing.[^3] Saudi airstrikes killed 7 UAE-backed forces.[^11] Two GCC allies conducting operations against each other’s proxies.

* Israel-Hezbollah Ceasefire Eroding: 10,000+ documented violations. Extended to February 18 but fundamental disagreements persist.

* Syria-Turkey Integration: Defense pact negotiations advancing. Turkish airbases discussed. Turkey displacing Iran as primary external influence.

* Netanyahu at Mar-a-Lago: New Year’s Eve meetings with Trump and Christian Zionists.[^15] Lobbying for Iran action.

Outlook Assessment

* 30-day: Iran protest trajectory critical. 45% confidence in stability maintenance.

* 60-day: Ceasefire faces February 18 pressure. 40% confidence.

* 90-day: Iran response to marginalization—accommodation or confrontation. 35% confidence.

Investment Considerations: Israeli defense (Elbit) provides escalation hedge. Oil call spreads for Iran scenarios. Gulf sovereigns carry Saudi-UAE fracture risk—consider reducing exposure. Avoid Lebanese assets entirely.

Asia-Pacific

Stability Index: 5/10 (▼ -1 vs. December)

Key Developments

* China-Taiwan Exercises: December 30-31 drills largest since August 2022 Pelosi visit.[^24] Missiles launched, dozens of fighters deployed. Xi declared reunification “unstoppable.”

* Japan Record Defense Budget: ¥9T ($58B)—9.4% increase, fourth consecutive buildup.[^25] PM Takaichi stated military “could get involved” if China acts.

* Taiwan Defense Pledge: President Lai called for $40B increase.[^26] “2026 will be a crucial year for Taiwan.”

* Radar Lock Incident: Chinese aircraft locked radar on Japanese aircraft[^25]—potential preparation for missile firing. Significant escalation in operational friction.

Outlook Assessment

* 30-day: Elevated tension following exercises. 65% confidence in stability (down from 80%).

* 60-day: 2027 readiness deadline creates ongoing pressure. 60% confidence.

* 90-day: Spring may see additional exercises. 55% confidence.

Investment Considerations: Japanese defense contractors (MHI, Kawasaki Heavy) benefit from ¥9T budget. TSMC carries elevated geopolitical risk premium but remains critical. China exposure requires significant risk tolerance given trade tensions and Taiwan dynamics.

Latin America

Stability Index: 2/10 (▼▼▼ -3 vs. December) — CRISIS LEVEL

Key Developments

* US CAPTURES PRESIDENT MADURO: In unprecedented military operation (January 4-5), US special forces seized Venezuelan President Nicolás Maduro and First Lady Cilia Flores in Caracas.[^30] Both arraigned in NYC on narco-terrorism charges. First US capture of sitting head of state since Noriega (1989).

* Venezuela Under Martial Law: Armed forces fully mobilized. Oil and key industries under military control.[^31] Power vacuum emerging. Oil production (~800k bpd) at risk.

* Regional Condemnation: Brazil, Colombia, Mexico oppose the operation. ECOWAS condemned violation of sovereignty.[^36] UN Security Council emergency session. Russia calls it a “crime.”[^32]

[CHART: International Response to Venezuela Operation - World map with color-coded country positions: Red (condemn: Russia, China, Cuba, Nicaragua, ECOWAS), Yellow (concern: Brazil, Colombia, Mexico), Green (support: unclear), Gray (no statement). Include key quotes from each bloc.]

* Mass Protests: Demonstrations outside NYC courthouse and in London. Only 33% of Americans approve per Reuters/Ipsos.[^34]

* Market Reaction: Chevron +6.7% on market open. Investor made $400k on Maduro fall bet (WSJ).[^37] Markets anticipate access to world’s largest oil reserves.

[CHART: Venezuela Crisis Timeline - Horizontal timeline showing: Dec 31 “Shadow War” begins → Jan 4-5 Maduro captured → Jan 5 NYC arraignment → Jan 5 Martial law declared → ? Transition scenarios.]

Outlook Assessment

* 7-day: Power vacuum, military council control likely. Oil disruption. Regional condemnation but no military response. Confidence: 80%

* 30-day: Transition government formation or continued instability. Oil production 20-40% below normal. Confidence: 50%

* 90-day: Managed transition (35%), prolonged instability (40%), regional contagion (15%), international isolation (10%). Confidence: 40%

Investment Considerations: Venezuelan assets completely uninvestable—active crisis. LatAm equities face severe contagion risk—reduce exposure by 25%. Brazilian equities particularly vulnerable given border proximity and diplomatic tensions. Mexican nearshoring thesis intact but monitor for spillover. Argentine reforms under Milei insulated but not immune. Consider oil call spreads for Venezuelan supply disruption.

Africa

Stability Index: 3/10 (▼ -2 vs. December) — SEVERE DETERIORATION

Key Developments

* Sudan Approaching 1000 Days: IRC #1 Emergency Watchlist.[^28] 150,000+ killed, 13M displaced. US determined RSF committed genocide. Drone attack on preschool killed 116 including 46 children.

* Sahel Coups Spread: Guinea-Bissau coup, Benin attempt. JNIM “economic warfare” in Mali. Burkina Faso 55%+ of extremist fatalities.

* France Withdrawal Complete: Full exit from West Africa—Senegal July 2025. Ends permanent French military footprint.

* Russia Port Sudan Suspended: Kremlin suspended naval base due to instability.[^29] Security vacuum widening.

* Israel-Somaliland Recognition: First UN member recognition (December 26).[^7] Creates precedent for Ethiopia. Connects Horn to Red Sea/Houthi dynamics.

Outlook Assessment

* 30-day: Sudan famine continues. 55% confidence in stability (down from 70%).

* 60-day: Sudan-South Sudan conflict convergence risk (RSF seized Heglig oilfield). 50% confidence.

* 90-day: Climate compounds food security. AES joint battalion effectiveness unclear. 45% confidence.

Investment Considerations: Avoid Sudan-adjacent exposure entirely. Nigerian oil carries elevated risk from regional instability. Sahel-exposed assets (Mali gold mining) face operational and security challenges. Kenya and East Africa offer better risk-adjusted opportunities. South African exposure remains viable for diversified continental access.

Phase 6: Risk Matrix

Risk Event Analysis

Note: US-Iran confrontation probability raised from 10% to 15% following Maduro operation—pattern of unilateral action established.

[CHART: V9 Risk Matrix Scatter Plot - Probability vs Impact scatter with Venezuela risks (Prolonged Instability, Oil Collapse, Contagion) prominently placed in high-probability/high-impact quadrant. Use larger markers for Venezuela risks. Include risk labels and color coding by region.]

Phase 7: Market Implications

Overweight Recommendations

Underweight Recommendations

Hedge Strategies

Trigger-Based Recommendations

Volatility Expectations

[CHART: V9 Implied Volatility Comparison - Bar chart showing implied vol by asset class, with Chevron (42%) and LatAm (38%) highlighted as new additions. Compare to V8 baseline where applicable. Use red/amber/green color coding for risk levels.]

Portfolio Construction Notes

* Maintain balanced book ahead of Kremlin response—binary outcomes create whipsaw risk

* Options structures (straddles, strangles) capture volatility without directional exposure

* Iran/Yemen developments may dominate news despite Ukraine settlement focus

* Fed stress introduces domestic US risk—monitor REPO operations for escalation

* Consider 10-15% cash/short-duration allocation for tactical deployment post-clarity

Phase 8: Methodology & Limitations

Methodology

This assessment synthesizes intelligence from 355+ monitored sources processed through automated pipeline with manual synthesis. Key analytical frameworks:

* Probability assessment: Bayesian updating with calibrated confidence intervals and diminishing returns for repeated signals

* Regional stability: 1-10 index incorporating political, economic, security, and social factors

* Risk matrix: Impact × probability assessment with specific asset implications and sizing

* Scenario analysis: Base case, alternative, and tail risk frameworks with portfolio implications

Known Limitations

* Iran coverage emerging: Protest situation evolving rapidly; assessments may lag developments by 12-24 hours

* Yemen opacity: Saudi-UAE dynamics poorly sourced in English-language channels; Arabic sources not systematically monitored

* Congressional dynamics: Ratification politics difficult to assess from open sources; relies on public statements

* Fed interpretation: REPO operations may reflect technical year-end factors vs. systemic stress; causation uncertain

* Pipeline gaps: Sahel depth limited, Syria/HTS coverage emerging, EU politics improving with new sources

Update Frequency

* Real-time: Pipeline-generated alerts on trigger events (110 alerts this period)

* Weekly: Comprehensive development review (ongoing)

* Monthly: Full strategic outlook (this report)

Disclaimer

This report is for informational purposes only and does not constitute investment advice. All investments carry risk, including potential loss of principal. Past performance does not guarantee future results. Geopolitical analysis involves inherent uncertainty; probability estimates are analytical judgments subject to significant error. Readers should conduct independent due diligence and consult qualified advisors before making investment decisions.

The author may hold positions in assets discussed. Source verification follows dual-confirmation standard where possible; single-source claims are noted.

Footnotes

[^1]: Zelensky New Year Address, BBC/Slavyangrad/multiple sources, January 1, 2026. Zelensky confirmed “90% of 20-point peace plan agreed” with security guarantees “100% in writing.”

[^2]: Iran protests spread to multiple cities, RFE/RL, BBC, geopolitics_prime, December 30, 2025-January 2, 2026. Multiple sources confirm protests in Hamedan, Tehran, and other cities with fatalities reported.

[^3]: UAE terminates Yemen counter-terrorism teams, Al Mayadeen, Guardian, France24, January 1-2, 2026. UAE Ministry of Defense announced formal end to Yemen military presence.

[^4]: Bulgaria joins eurozone as 21st member, Euronews, ECB Press Release, January 1, 2026. https://www.ecb.europa.eu/press/pr/date/2026/html/ecb.pr260101.en.html

[^5]: Philip Gordon urges Zelensky to reject Trump plan, Slavyangrad, January 2, 2026. Former Harris security advisor argues US guarantees “will not be implemented.”

[^6]: Fed REPO operations, myLordBebo, CIG_telegram, financial sources, January 1-2, 2026. Federal Reserve injected $31B+ via REPO facility; cumulative recent injections exceed $74.6B.

[^7]: Israel recognizes Somaliland, allafrica, Al Jazeera, December 26, 2025. Israel became first UN member state to formally recognize Somaliland independence.

[^8]: Hamedan protests turn deadly, geopolitics_prime, RFE/RL, January 1, 2026. Protesters burned Qurans and prayer books; security forces responded with force; multiple fatalities.

[^9]: Trump: US ready to fight for protesters, BBC World, nhkworld, January 1, 2026. Trump stated US is “locked and loaded” and ready to “fight for” Iranian protesters.

[^10]: US satellite activity over Iran increases, rybar_in_english, January 2, 2026. Rybar analysis detected increased American ISR activity over Iran.

[^11]: Saudi airstrikes kill UAE-backed forces, CIG_telegram, Guardian, January 2, 2026. Saudi-backed “Homeland Shield Forces” launched operations; airstrikes killed 7 STC forces.

[^12]: 49% of Bulgarians opposed euro adoption, Euronews, January 1, 2026. Public opinion polling showed plurality opposition despite adoption proceeding.

[^13]: Russia rejects ceasefire proposal, Slavyangrad, rybar_in_english, sitreports, December 31, 2025-January 2, 2026. Kremlin stated it is “formulating response” to 20-point plan while rejecting 60-day ceasefire.

[^14]: Students join Iran protests, RFE/RL, January 2, 2026. University students joining protests expands base beyond initial economic grievances.

[^15]: Netanyahu at Mar-a-Lago, Middle East Eye, January 1, 2026. Netanyahu spent New Year’s Eve with Trump, met with Christian Zionist leaders.

[^16]: Khamenei: Iran in full war with US, Israel, Europe, presstv_Iran, FotrosResistancee, January 1, 2026. Supreme Leader’s rhetorical escalation framing domestic unrest as external aggression.

[^17]: Saudi-UAE tensions reach boiling point, Guardian World, January 2, 2026. https://www.theguardian.com/world/2026/jan/02/saudi-uae-yemen-tensions

[^18]: 205-drone New Year attack on Ukraine, European_dissident, rybar_in_english, January 1, 2026. Largest single drone assault of 2026.

[^19]: Odessa semi-blockade, Wall Street Journal via sitreports, January 2, 2026. WSJ reports Russian economic stranglehold on Odessa tightening.

[^20]: Kherson café attack kills 27, multiple sources, December 31, 2025. New Year’s Eve attack on civilian gathering.

[^21]: Putin signs reserve mobilization decree, Slavyangrad, January 1, 2026. Decree authorizes reserve call-up for infrastructure protection.

[^22]: Oreshnik missiles enter active service, Defense News, January 2, 2026. Nuclear-capable hypersonic system deployed during peace talks.

[^23]: Starmer delays Defence Investment Plan, sitreports, FT, January 2, 2026. UK delayed defense plan over “affordability” concerns.

[^24]: China-Taiwan drills December 30-31, TheSimurgh313, nhkworld, multiple sources. Largest exercises since August 2022 Pelosi visit.

[^25]: Japan approves record ¥9T defense budget, Japan Times, nhkworld, December 28, 2025. 9.4% increase, fourth consecutive buildup year.

[^26]: Taiwan’s Lai calls for $40B defense increase, nhkworld, January 1, 2026. “2026 will be a crucial year for Taiwan.”

[^27]: Venezuela shadow war, Guardian, CNN, December 31, 2025-January 2, 2026. US deployed 4,500 troops; first ground-target strike since Panama 1989.

[^28]: Sudan #1 on IRC Emergency Watchlist, Middle East Eye, IRC report, January 1, 2026. 150,000+ killed, 13M displaced, genocide determination.

[^29]: Russia suspends Port Sudan base, sitreports, Small Wars Journal, January 2026. Kremlin suspended naval base plans due to instability.

[^30]: US captures Maduro in military operation, Al Mayadeen English, Press TV, multiple Telegram sources, January 4-5, 2026. US special operations forces seized Venezuelan President Nicolás Maduro and First Lady Cilia Flores in Caracas; both transported to NYC for arraignment on narco-terrorism charges.

[^31]: Venezuela declares martial law, Al Mayadeen English, Two Majors, January 5, 2026. Venezuela orders full military mobilization, places oil and key industries under temporary military control.

[^32]: UN Security Council emergency session on Venezuela, Press TV, Two Majors, January 5, 2026. Russia’s UN Ambassador Nebenzya condemned US action as a “crime” violating international law.

[^33]: Chevron shares surge 6.7%, Azazel News, ZeroHedge, January 5, 2026. Chevron shares rose immediately on US market open following confirmed Maduro capture.

[^34]: Only 33% of Americans approve Venezuela operation, Frontline Report citing Reuters/Ipsos, January 5, 2026.

[^35]: “Maduro didn’t know they were coming until three minutes before”, Lord Bebo, January 5, 2026. Defense Secretary Hegseth statement on operation timing.

[^36]: ECOWAS condemns Venezuela operation, Press TV citing Al Mayadeen, January 5, 2026. West African bloc calls for respect of Venezuela’s sovereignty.

[^37]: Investor earned $400,000 betting on Maduro fall, Frontline Report citing Wall Street Journal, January 5, 2026. Unknown investor profited from futures market bet on regime change.

[^38]: Cilia Flores appeared with injuries, The Simurgh Chat, January 5, 2026. Maduro’s wife appeared in court with bandage on forehead and bruising near right eye.

Source Methodology

This assessment synthesizes intelligence from 355+ monitored OSINT sources including wire services, regional specialists, defense publications, financial signals, and real-time intelligence channels.

All major analytical claims are verified against multiple sources where possible. Single-source claims are explicitly noted. OSINT sources provide early indicators that often precede mainstream coverage by 6-24 hours.

PREPARED BY: TATSU Geopolitical IntelligenceVERSION: V9 (Breaking Update — Maduro Capture)SOURCES: 355+ OSINT channelsEVENTS ANALYZED: 1,307 (Venezuela-specific scan) + 887 (pipeline)ALERTS GENERATED: 118DISTRIBUTION: Institutional Clients OnlyNEXT UPDATE: February 2026 (or sooner if Venezuela situation evolves significantly)CONTACT: For custom research requests or briefing calls, contact: tatsu [at] tikeda dot com