It Actually Does “Work” For Shareholders

When the Economy Isn’t Working

The Hidden Logic Behind Unemployment, Inflation, and Financialized Wealth

Conventional economic wisdom treats unemployment and inflation as straightforward negatives: unemployment means despair and wasted human potential; inflation means eroded purchasing power. But when you see the economy through the lens of distribution and power, a counterintuitive pattern emerges:

Unemployment weakens workers, suppresses wages, and redistributes economic rents upward — largely into the hands of financial capital and corporate profits.

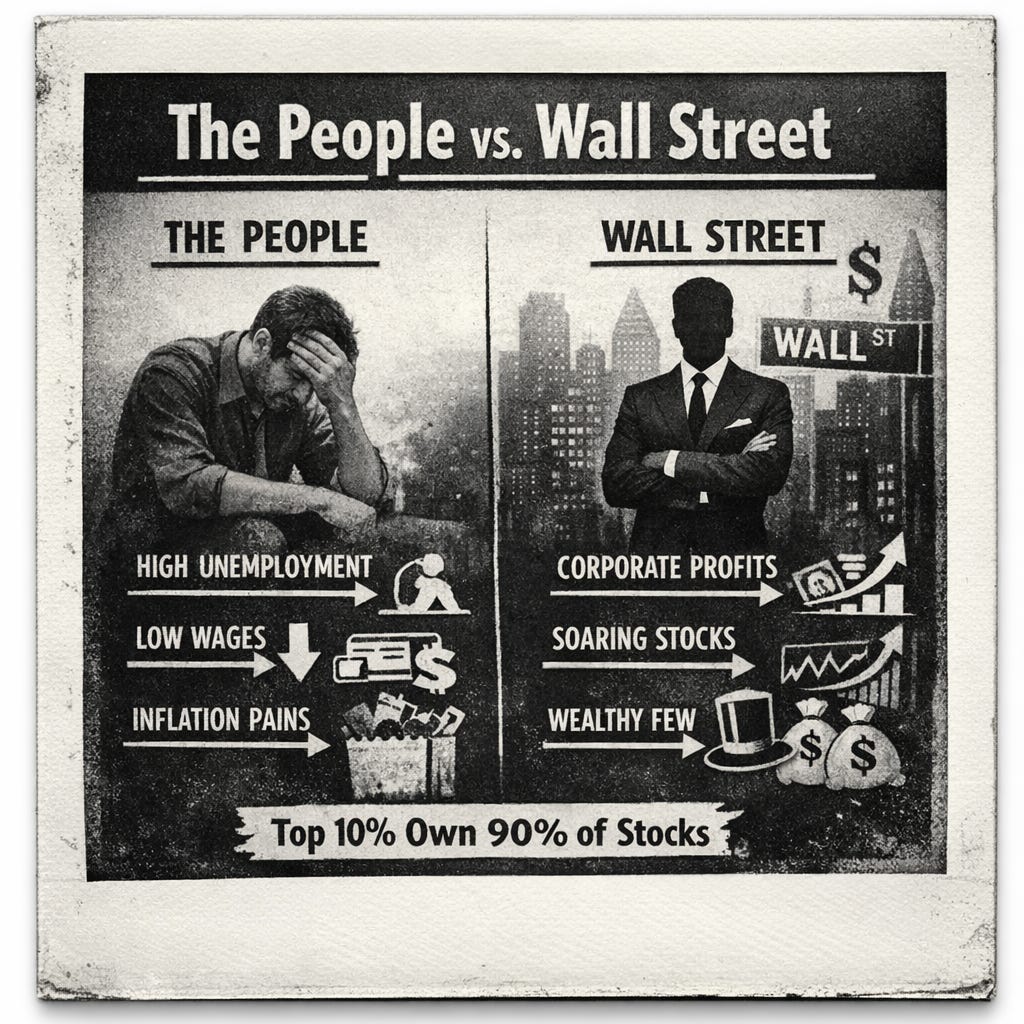

1. Unemployment Isn’t Just a Statistic — It’s a Lever Against Wages

Economists have long observed an inverse relationship between unemployment and wage growth — the so-called Phillips curve. When unemployment is high, workers have less bargaining power; wage inflation is muted, and employers can keep labor costs lower. When unemployment is low, historical theory says wages rise faster.

In practice over recent decades, that relationship has flattened — but the intuition remains: labor slack limits wage growth. Firms don’t have to bid for workers; they get them cheap. Wage suppression translates into higher profit margins and, in an era of financialization, more cash available for dividends and buybacks — mechanisms that benefit asset holders

.

2. Stock Market Gains and “Paper Wealth” Are Concentrated at the Top

Here’s where the fundamental redistribution happens: virtually all paper gains from economic policy accrue to those who own the assets — not those who earn wages.

* The top 1% own roughly half of all U.S. equities, with the next ultra-wealthy controlling another large slice, while the bottom half of households own essentially none.

* Another credible estimate puts the top 10% of households at ~93% of all stock market wealth; the bottom 50% hold just ~1%.

This is not a quirk — it’s structural. Asset ownership is concentrated, and asset price appreciation (stocks, private equity, real estate) is the main vehicle through which modern monetary and fiscal policy transmits “growth.”

When corporations see cheap labor, weak wage pressure, and accommodative monetary policy they don’t just make widgets — they load up on financial engineering, stock buybacks, and dividends that send returns straight to the investor class.

That’s why stock markets can rise even while broad economic insecurity persists: market gains and macroeconomic stress are not mutually exclusive.

Buy Me A Coffee

3. Inflation Isn’t Just a “Tax on the Poor.” It Redistributes In Complex Ways

Inflation is popularly condemned as destroying living standards — but it doesn’t do so uniformly:

* People with fixed nominal incomes (e.g., pensions that are not fully indexed) are harmed because their purchasing power erodes.

* People with variable incomes or asset holdings often see nominal gains that at least partially offset price increases.

* Those who own financial assets — like stocks or real estate — often benefit from inflationary periods because asset prices tend to rise with or above general price levels.

In effect, inflation can act as a vehicle for redistribution: reducing the real value of debts for debtors, allowing firms to maintain nominal growth, and encouraging employers to hire more workers when they anticipate future price increases (because tomorrow’s output will be worth more).

Academic work shows that the impact of inflation on wealth inequality isn’t linear — at moderate levels it can reduce top shares slightly; above certain thresholds inequality begins rising again, especially through asset price effects.

4. So Who Actually Wins When “The Economy Isn’t Working”?

A sober, data-anchored mapping looks like this:

Winners:✔ Corporate management (profits and retained earnings)✔ Financial asset holders (equities, private equity, real estate)✔ Institutions with capital to deploy (banks, funds, sovereign investors)

Losers:✘ Unemployed workers (no wages, rising cost pressures)✘ Wage-dependent earners during downturns✘ Fixed-income seniors without full inflation indexing✘ Small savers whose savings don’t beat inflation

This dynamic emerges from decades of policy choices — monetary easing focused on asset prices, deregulated financial markets, and tax frameworks that favor capital gains. These have generated rich stock market returns without proportionate wage growth for ordinary workers. It’s why inequality has grown, not shrunk.

A Story of Redistribution, Not Simple Failure

Viewed as a ledger of winners and losers, the “bad” economy reveals its logic: unemployment weakens labor; subdued wage gains boost corporate margins; inflation transfers value toward variable income streams and assets; and stock market gains disproportionately enrich those who already own the market.

This isn’t accidental. It’s the outcome of a financialized macroeconomic order that equates rising asset prices with economic success — even when most people never see those gains in their paychecks or in their ability to buy groceries.

If your definition of success is Wall Street up, Main Street down, then unemployment and inflation can be said to “work.” But if success means shared prosperity, rising wages, and broadly distributed wealth — the current system is, by design, working against that.

Footnotes

[1] A.W. Phillips, “The Relation Between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861–1957,” Economica, 1958.Foundational paper establishing the inverse relationship between unemployment and wage growth, later adapted into modern labor-market analysis.

[2] Federal Reserve Bank of St. Louis (FRED), Real Median Weekly Earnings and Unemployment Rate datasets.Long-term data shows suppressed wage growth during periods of elevated unemployment despite rising productivity.

[3] William Lazonick, “Profits Without Prosperity,” Harvard Business Review, September 2014.Documents how corporations increasingly allocate profits to stock buybacks rather than wages, hiring, or productive investment.

[4] Federal Reserve, Distributional Financial Accounts of the United States (DFA), latest release.Shows that the top 10% of households own approximately 90% of U.S. corporate equities and mutual fund shares, while the bottom 50% own ~1%.

[5] Edward N. Wolff, “Household Wealth Trends in the United States, 1962–2019,” National Bureau of Economic Research (NBER).Confirms extreme asset concentration and links wealth inequality to financial asset ownership rather than labor income.

[6] Olivier Blanchard, “Public Debt and Low Interest Rates,” American Economic Review, 2019.Explains how moderate inflation can reduce real debt burdens and stimulate employment without immediate harm to growth.

[7] Jason Furman & Lawrence Summers, “Who’s Afraid of Inflation?” Peterson Institute for International Economics, 2020.Argues that modestly higher inflation can improve labor-market outcomes and wage growth, especially for lower-income workers.

[8] International Monetary Fund (IMF), “Inflation and Income Inequality,” Staff Discussion Note, 2022.Finds that moderate inflation combined with strong employment can reduce inequality, while unemployment amplifies it.

[9] Federal Reserve Bank of Dallas, “Wage Rigidity and Inflation,” Economic Commentary.Shows that low inflation environments increase real wage rigidity, discouraging hiring and reinforcing labor market slack.

[10] U.S. Bureau of Labor Statistics (BLS), Employment Cost Index and Consumer Price Index.Demonstrates that workers without jobs or with fixed nominal incomes suffer most during inflationary periods, while employed workers with COLA adjustments fare better.

[11] Center on Budget and Policy Priorities (CBPP), “Income Inequality and the Concentration of Wealth,” updated briefing.Tracks how capital income (dividends, capital gains) has grown far faster than wage income since the 1980s.

[12] Thomas Piketty, Capital in the Twenty-First Century, Harvard University Press.Establishes the structural dominance of capital returns over labor income when policy favors asset appreciation.