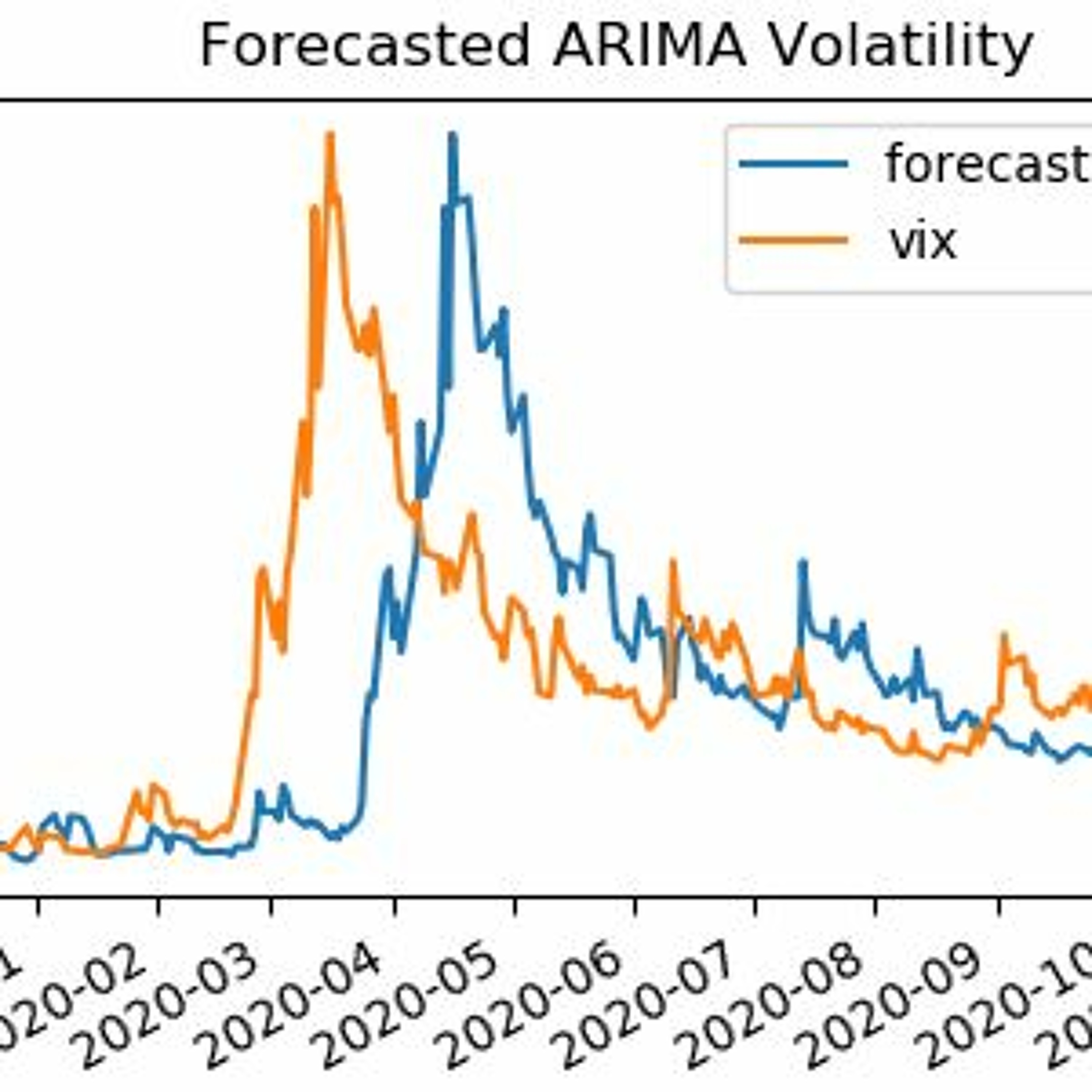

In a previous post, we presented theory and a practical example of calculating implied volatility for a given stock option. In this post, we are going to implement a model for forecasting the implied volatility. Specifically, we are going to use the Autoregressive Integrated Moving Average (ARIMA) model to forecast the volatility index VIX.

http://tech.harbourfronts.com/trading/forecasting-implied-volatility-arima-model-volatility-analysis-python/