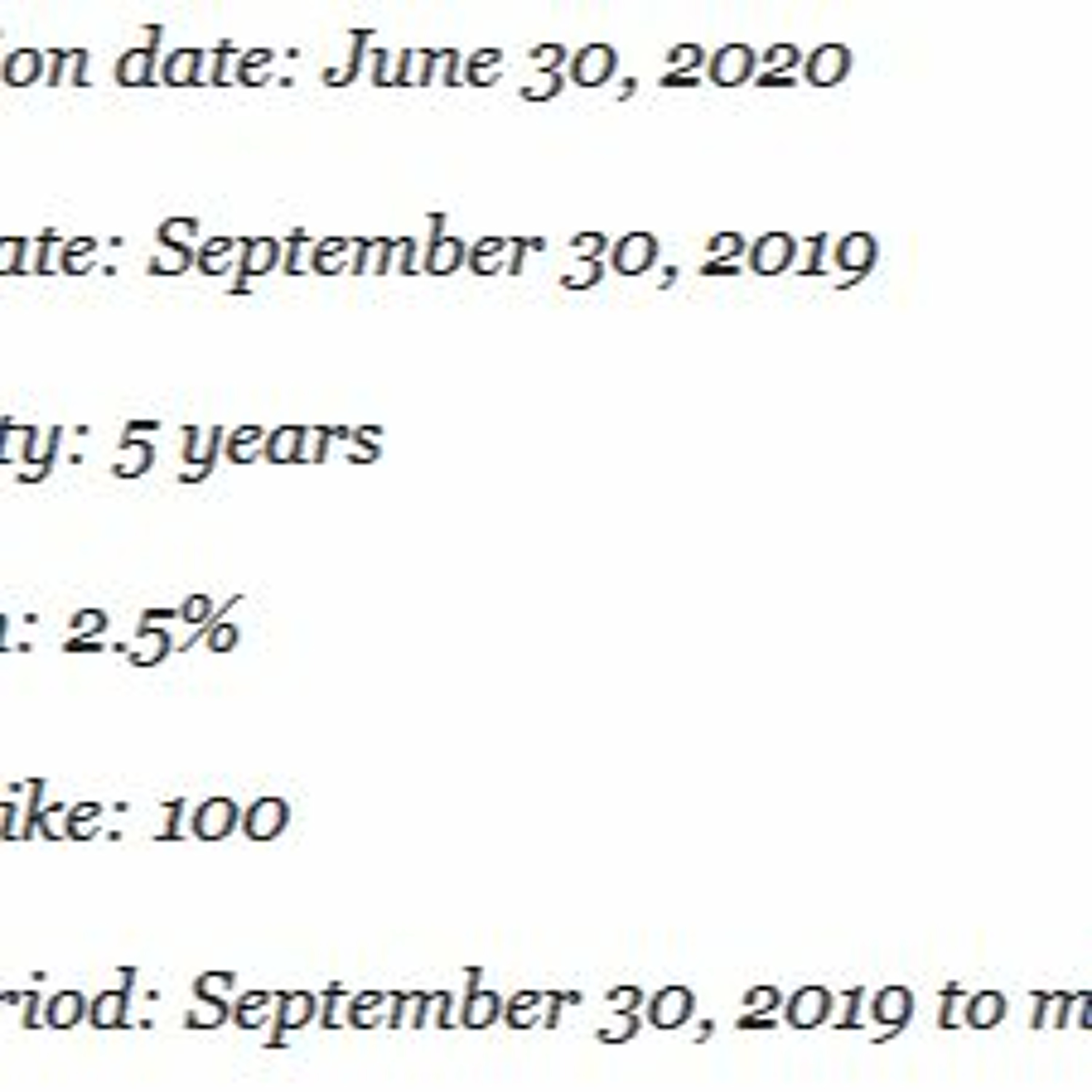

We are going to discuss valuation of a callable bond. We chose the Hull-White model to describe the interest rate dynamics. We then use a Python program to build a trinomial tree for the risk-free rates

http://tech.harbourfronts.com/derivatives/valuation-callable-puttable-bonds-derivative-pricing-python/